Online advertising giant Alphabet Inc (NASDAQ: GOOG), the parent company of Google, reported Q1 FY2023 results that exceeded Wall Street’s expectations.

Alphabet’s revenue rose 3% year-on-year (yoy) to US$69.79 billion from US$68 billion a year earlier. This surpassed analysts’ expectations of US$68.9 billion, based on Refinitiv data.

Meanwhile, net income was down slightly to US$15.05 billion, or US$1.17 per share, from US$16.44 billion, or US$1.23 per share in the year-ago period. This was better than the earnings per share (EPS) of US$1.07 expected by analysts.

This is the first time Alphabet’s financial performance beat analysts’ expectations after four straight quarters of underperformance against Wall Street’s estimates.

However, despite that, the overall performance is mixed as Alphabet’s core ad business posted a decline in revenue.

So, is it a good time for investors to buy Alphabet’s shares now as financial results surpassed analysts’ expectations?

After all, the share price of Alphabet is still down by 5.9% over the past year.

I’ll take a look at these key developments to see if it’s worth the risk to invest into the search engine giant.

1. Google Cloud drives revenue growth

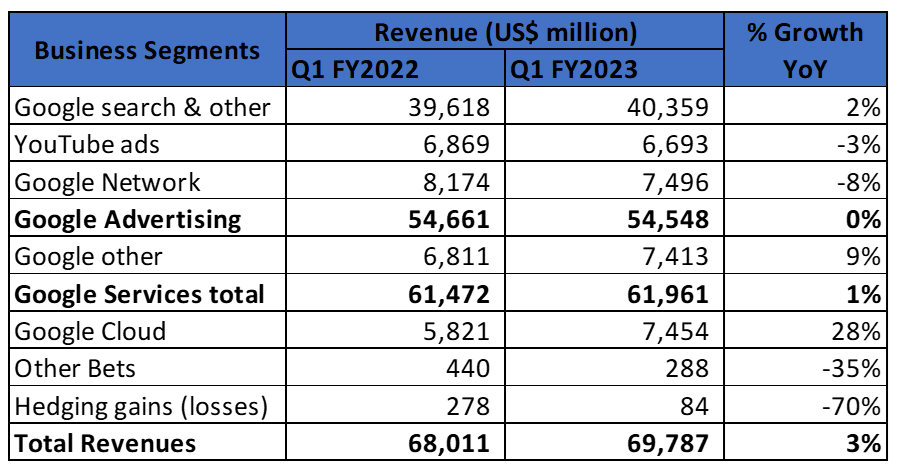

Alphabet’s revenue grew 3% yoy during Q1 FY2023, mainly driven by Google Cloud (+28% yoy). Google search and Google other also contributed to the growth.

However, Google’s advertising business was down slightly during the quarter at US$54.5 billion. This was still better than the US$53.8 billion expected.

It is also worth noting that YouTube advertising revenue was down by 3% yoy in Q1 FY2023.

Source: Alphabet’s Q1 FY2023 Financial Highlights

2. Alphabet’s cost-cutting measures will boost margin in the long term

Despite Alphabet pushing itself to become more efficient, operating margin was 25%, down from 30% a year ago.

Similar to other technology players, Alphabet has been cutting costs aggressively.

In January, Alphabet announced a cut of 12,000 jobs.

This has led to a decline in its margin in the near term with US$2.6 billion in charges related to employee layoffs and a reduction in office space.

Operating income for Q1 FY2023 was down by 13% to US$17.4 billion.

One positive takeaway is the turnaround in Google Cloud, which turned an operating profit of US$191 million during the quarter as compared to its operating loss of US$706 million a year ago.

3. Alphabet authorises US$70 billion share buyback

Alphabet announced that it would buy back US$70 billion worth of stock.

No specific timeline was given but Alphabet spent around US$14.5 billion on share buybacks during the first quarter.

The share price of Alphabet rose as much as 5% in after-hours trading as investors cheered the buyback plan.

4. Alphabet restructures its AI teams to compete

Google has found itself at the epicentre of a burgeoning AI rivalry, which was ignited by ChatGPT’s ascent, transforming this technology into the tech sphere’s latest growth impetus.

Over the past several months, Google’s AI prowess has been met with skepticism, as their AI chatbot, Bard, has underwhelmed.

In contrast, Microsoft Corporation (NASDAQ: MSFT) and its substantial investment in OpenAI — the creator of ChatGPT — have garnered significant public interest.

In response to the evolving landscape, Google is implementing numerous modifications to its AI strategy by merging its two AI divisions, Google Research’s Brain unit and DeepMind.

This strategic shift was evident during the financial results briefing, which disclosed AI-related expenses separately from Alphabet’s Other Bets segment, for the first time.

During Q1 FY2023, losses attributed to the company’s AI endeavours amounted to US$3.3 billion, while the Other Bets segment experienced a US$1.23 billion deficit.

Decent results but more work left to do for Alphabet

Alphabet reported decent results for Q1 FY2023 given the challenging environment for its core ad business.

However, the recovery remains uncertain with a potential recession in the US.

The company has been proactive in managing its costs through employee and office space downsizing, which should boost margin in the longer term.

Another challenge is the threat to its Google search business with the rise of ChatGPT.

Competition in the AI space remains intense and while Alphabet has restructured its AI business teams, more work is left to do for the company.

Alphabet is a great investment opportunity for investors who love its search engine business but with so much uncertainty in the horizon, I believe there are other (better) tech stocks with lower risk to buy right now.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.