■ The Dollar Index (DXY) soften slightly but not amounting to a reversal yet despite PCE soften to 2.6% from 2.8% in April 2024.

■ The AUD may have gained through the possible play of dovish Fed but the main push is the hawkish Reserve Bank of Australia (RBA) and its sharp increase in inflation to 4%.

■ There is also a possibility that the Australian may hike interest rate after a hiatus.

Dollar Index soften on declining PCE number

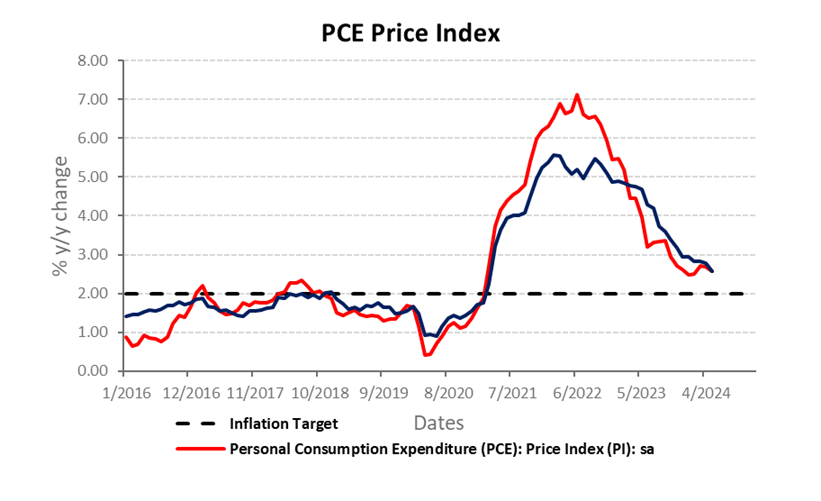

The US Personal Consumption Expenditures (PCE) Price Index for report for May showed that headline inflation softened to 2.6% year-over-year, down from 2.7% in the previous month. Core PCE, which excludes the more volatile food and energy prices, also experienced a decline, dropping to 2.6% from April’s 2.8%. The in-line numbers has promoted the market that the Fed is likely back on track to further rate cut for 2H24, from one cut to two. However, we believe that the rate cut scenario is unlikely to come as other Fed committee members such as Austan Goolsbee, and Mary Daly has expressed the need for more data to see inflation coming back to 2%. We believe that this coming Thursday’s FOMC (0200hrs GMT+8) will likely maintain its stance on “more data needed” and not have any surprise as unemployment data on Friday will be the key. Unemployment is likely to maintain at 4% based on consensus but NFP may show a dip to 180,000 based on consensus view.

RBA back into possible rate hike

While the rest of the major economies such as the Eurozone, United Kingdom, and United States saw a decline in inflation, Australia is seeing a strong consecutive surge in inflation, especially the latest data showing a strong surge towards 4%. This not only dashes the hope of a rate cut but also fuels the chance of a rate hike. While RBA has noted that more incoming data is needed, the current sentiment is seeing a possibility of a status quo. As such, the Aussie dollar may continue to see strength going forward and may be a strong contender against the mighty US dollar.

Dollar Index technical outlook

We continue to maintain our view of a strong dollar despite softening last Friday after the result of the PCE numbers. The Dollar index has briefly broken past the 106.00 psychological level and despite the weak closure, the Dollar did not exhibit a strong bearish reversal. Furthermore, the momentum also suggests that the upside remains and hence, we maintain our mid-term target at 106.74 and should it break, the next major target will be at 109.49 over the longer course of the period. Major support is at 103.86-104.10 and 101.31 should there be a correction.

AUDUSD’s resistance at 0.6670 may be broken

The AUDUSD has been forming a series of higher lows since bottoming out on 13 Oct 2022. While the major downtrend line of 3 years has yet to be broken, the AUDUSD’s near-term uptrend is back after prices have successfully trended above all the ichimoku indicators. Furthermore, the consolidative range between 15 May to 24 June 2024 is likely a bullish continuation pattern as the resistance at 0.6670 has been weakened due to multiple testing. Hence, should it break out successfully, our near-term target will be at 0.6784. Key support will be at 0.6500 should there be any correction.

Figure 1:Dollar Index (DXY) – Short-term uptrend remains as bearish pressure is weak

Figure 2:AUDUSD – Testing the weakened resistance at 0.6670

Figure 3: Personal Consumption Index – PCE declined but yet to achieved 2% target

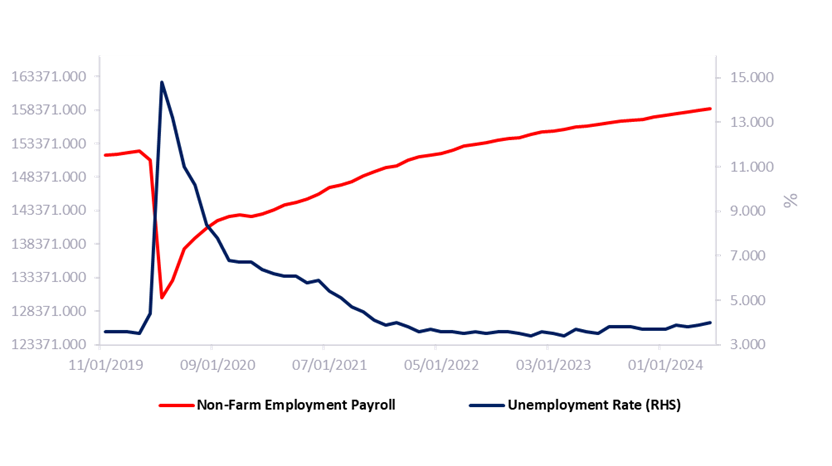

Figure 3: Unemployment rate – Inching closer to 4.2% Natural rate of unemployment

Please refer to the disclaimer here.