Stock markets in the US may have been roiled this week by higher, and no longer transitory, inflation and its impact on interest rates.

In Singapore, though, stock market movements have been relatively muted. Part of that is attributable to the simple fact that Singapore has few of the “growth” stocks that are adversely impacted by rising rates.

However, what the local market here does have is a lot of REITs. And as I covered earlier – in “Digital Core REIT IPO: Should Dividend Investors Buy Shares” – the REIT market is still in rude health given ultra-low yields.

That was perhaps no better exemplified than by Mapletree Logistics Trust’s (SGX: M44U) announcement earlier last week that it intended to acquire 17 properties in China, Vietnam and Japan for a combined S$1.4 billion.

While the logistics-focused REIT – which is backed by Mapletree Investments Pte Ltd – had a solid earnings report in late October, it’s still looking to expand its portfolio in an ambitious manner.

Overall, 13 of the 17 properties are in China while three are in Vietnam and one in Japan. All the properties are also very new, with a weighted average age of just 1.5 years.

All that means Grade A specifications and favourable characteristics for companies looking to hire out space in modern logistics facilities.

Riding structural tailwinds

It’s in this long-term logistics structural story, given the rise of e-commerce in Asia, that the REIT is trying to carve out a space for itself.

Post-acquisition, just over 30% of Mapletree Logistics Trust’s assets under management (AUM) will be in emerging Asian markets versus just 25% pre-acquisition.

It clearly sees a lot of growth in demand in developing Asian markets. One, e-commerce and logistics space will continue to be in demand as online retail continues to take market share of overall retail.

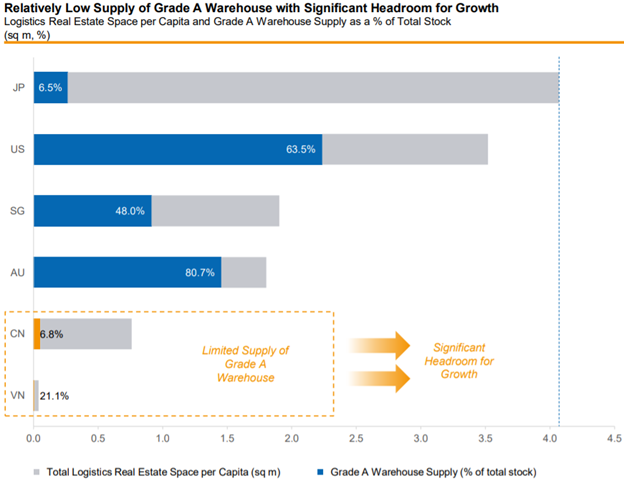

Second, and probably even more important, is the fact that Grade A warehouse space is in short supply in all three markets.

China and Vietnam already have one of the lowest “total logistics real estate space per capita” in Asia while the percentage of Grade A space in both China and Japan is well below 10% (see below).

Both factors should provide tailwinds for rents over the longer term. In fact, Mapletree Logistics Trust says that the average rent premium for Grade A space versus traditional warehouses in China can range from 25-30%.

While many bigger Singapore REITs continue to acquire to become even larger, it’s worth remembering that investors should watch out for the all-important distribution per unit (DPU) growth over the medium to long term.

Sources: Mapletree Logistics Trust presentation as of 22 November 2021, independent market research consultants

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips owns shares of Mapletree Logistics Trust.