While investors in US stock markets work themselves up over higher inflation and interest rates, here in Asia the focus for investors is on China, its economy and its tech giants’ fortunes.

Recently, the stocks of the Chinese tech giants have fared less well as a regulatory crackdown from the government has been both persistent and ruthless.

Well, for long-term investors, there has been some light shed on how their businesses have held up. Hong Kong-listed gaming and social media behemoth Tencent Holdings Ltd (SEHK: 700) reported its earnings a few weeks ago – which proved to be a mixed bag.

Last week, it was the turn of e-commerce, cloud computing and fintech giant Alibaba Group Holding Ltd (SEHK: 9988) (NYSE: BABA) to reveal its latest Q2 fiscal year (FY) 2022 results to investors.

Unfortunately, for current shareholders anyway, it wasn’t pretty. Alibaba shares, both in New York and Hong Kong, fell over 10% in response to the numbers.

Here’s what investors should know about the company’s latest results.

Slowing e-commerce growth

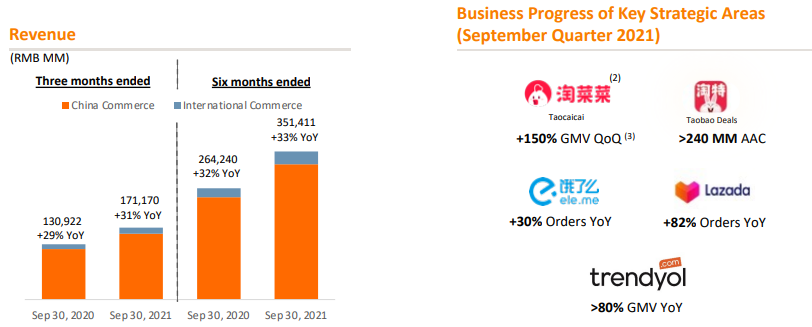

Alibaba missed consensus expectations on its revenue for the quarter, posting total consolidated revenue of RMB 200.7 billion (US$31.4 billion) – up 29% year-on-year.

However, excluding the Sun Art acquisition, growth was only 16% year-on-year. This was mainly down to a marked deceleration in customer management revenue (CMR) for its marketplace, which saw just a 3% year-on-year rise.

This was attributed to a slowing down in e-commerce growth in China as well as increased competition in the online space.

That’s no surprise as the likes of JD.com Inc (SEHK: 9618) (NASDAQ: JD) and Pinduoduo Inc (NASDAQ: PDD) have really stepped up their game, while newer entrants like Meituan Dianping (SEHK: 3690) – which is entering the grocery delivery field – are also starting to encroach on Alibaba’s turf.

International contribution still marginal

Its commerce business still makes up 85% of its overall revenue and while its international business is showing robust expansion, posting 34% year-on-year growth, it still only contributes 7% to total group sales.

More context is also needed. Lazada saw an 82% year-on-year bump in orders (see below) flowing through its platform.

At first glance that may seem impressive but key competitor Shopee – owned by Sea Ltd (NYSE: SE) – saw gross orders explode 123% to 1.7 billion for its own third quarter.

Given Shopee is the leading platform in Southeast Asia, and posted GMV of a whopping US$16.8 billion in the third quarter, investors can safely assume Shopee is growing orders faster than Lazada but off a much larger GMV base – given its leading position in multiple countries throughout the region.

That’s an indirect indictment of Lazada and how it continues to lag Shopee in terms of its strategy and execution.

Source: Alibaba Q2 FY2022 earnings slides

Lower guidance but cloud the silver lining

Alibaba also lowered its guidance for full-year revenue, previously expecting near-30% top line growth for its fiscal year 2022.

However, in Alibaba’s latest earnings release, the company lowered this percentage range to 20% to 23% revenue growth.

Meanwhile, non-GAAP net income of RMB 28.5 billion – down 39% year-on-year – compounded the misery on the top line.

However, its cloud computing arm continues to be the bright spot for Alibaba. Revenue for its cloud division was up 33% year-on-year to RMB 20 billion while it also delivered positive adjusted EBITDA of RMB 396 million – continuing to prove that cloud can build profitability as it scales.

Beware of bottom-fishing

Overall, investors should view Alibaba’s latest results as a possible harbinger of the competitive challenges that it faces in its core commerce business.

While Alibaba’s various platforms clearly have a massive collective user base – numbering 1.24 billion annual active customers (AAC) – it is facing stiff competition in its key home market of China.

Furthermore, its cloud division, while growing, is nowhere big enough to make up for any shortfall in the e-commerce space.

It appears that Alibaba – originally a disruptor in the e-commerce space – looks like it may be getting disrupted itself.

With Alibaba’s Hong Kong shares down 42% so far in 2021, and recently hitting a 52-week low, it might be advisable for long-term investors to wait and see whether it can turn around its business over the next six to 12 months.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips owns shares of Sea Ltd.