In the world of sportswear and fashion, investors have tended to favour US giant Nike Inc (NYSE: NKE). There’s good reason for that. Nike stock has been a formidable generator of long-term returns.

However, it’s also well-known that Nike is a giant already, with a market cap close to US$270 billion. Over the past five years, Nike’s share price is up nearly 190%.

Yet, over in China, where investors are consumed with the tech market sell-off, companies in other sectors are doing just fine.

While we’ve now realised that stock market returns in China are going to be partly dependent on government policy, one part of the Chinese economy that continues to thrive is the sportswear sector.

Why is this the case? Because the Chinese government wants to promote a more active lifestyle for its citizens, something it outlined in its latest five-year plan.

The 14th five-year plan (for 2020-2025) included creating or expanding 2,000 fitness venues – such as sports parks or stadiums – so that “full coverage” of fitness facilities is extended across the country.

That means that residents are within 15-minutes walking distance from a place of exercise. Unsurprisingly, that is going to create winners in the local sportswear industry.

Here’s one sportswear stock that long-term investors bullish on China can buy and hold.

Building China’s Nike

One of the biggest sportswear brands in China, that if often dubbed “China’s Nike, is ANTA Sports Products Ltd (SEHK: 2020). It also happens to be one of the world’s largest sportswear brands by revenue.

The company owns its own eponymous label as well as the highly-recognisable FILA brand. Together, the two core brands made up around 95% of Anta’s overall revenue in 2020.

Over the past five years, Anta’s share price is up over 720%, more than tripling Nike’s return. There are good reasons for that.

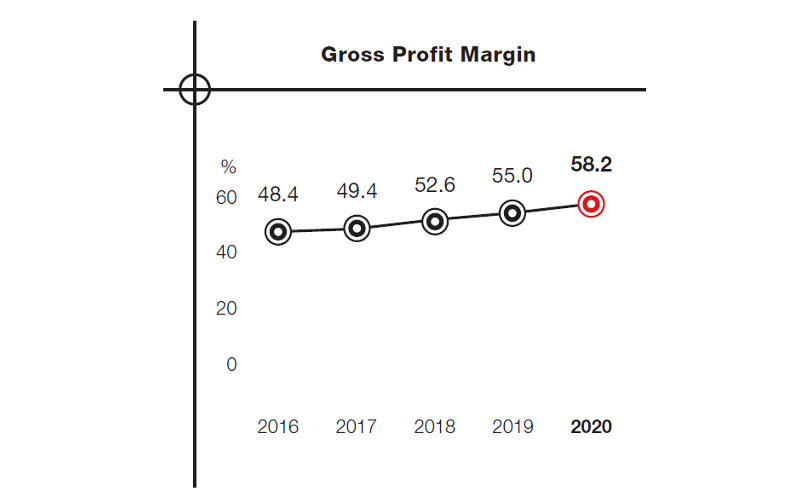

While Anta’s revenue was up only 4.7% year-on-year in 2020, its gross profit margin was up a whopping 320 basis points to 58.2%. As you can see from the chart below, Anta’s gross margin has been steadily rising since 2016.

Source: Anta Sports full-year 2020 earnings presentation

Source: Anta Sports full-year 2020 earnings presentation

This was mainly down to Anta going down the same route as Nike – building out its higher margin direct-to-consumer (DTC) retail model.

Instead of relying on marketplaces such as Alibaba Group Holding Ltd’s (NYSE: BABA) (SEHK: 9988) Taobao or Tmall, Anta has decided to start up its own visible brand online and get in front of consumers directly.

Patriotic consumption

That has also contributed to helping Anta build a strong, emotional bond with the Chinese consumer.

Playing on its Chinese roots, Anta was among the local sportswear brands that committed to continuing to use cotton sourced from Xinjiang in April of this year.

With international human rights concerns surrounding the use of forced labour in Xinjiang, it was a contentious issue that saw Western clothing brands, such as H&M, boycotted by Chinese consumers.

Anta went a step further by stating its intention to quit the Better Cotton Initiative (BCI), a Switzerland-based organization, so that it could go on sourcing cotton from Xinjiang.

In future, the trend is towards Chinese consumers favouring their own local brands. It’s this focus on “buying local” which bodes well for Anta sales in future.

Playing on the positive trends

For long-term investors who want to tap into the increasingly affluent Chinese consumer, Anta Sports offers a structurally positive way to play the trend.

That’s because China’s government will support the rise of a more active lifestyle while Chinese consumers are starting to prefer their own, homegrown brands as the quality of these goods now rival their Western counterparts.

Finally, Anta offer sportswear and fashion across different price points and demographics with its impressive brand campaigns.

This is one company for investors to keep on their watchlists if they’re aiming for a healthier, and more robust, China portfolio.

Disclaimer: ProsperUs Head of Content Tim Phillips doesn’t own shares of any companies mentioned.