Inflationary pressures were already elevated heading into 2022 amid supply chain disruptions, clogged ports, logistics strains and strong demand for goods.

As inflation continues to rise following the surge in gasoline prices amid the Russia-Ukraine war, investors need to buy into companies that can beat inflation.

Typically, these companies have two characteristics: strong pricing power and the ability to pay a dividend.

I think alcohol drinks giant Diageo PLC (LSE: DGE) helps investors to beat inflation and could even offer protection against the potential risk of stagflation.

Here are five reasons why I think investors can buy and hold Diageo in order to shield their portfolios against the risk of stagflation while also beating inflation.

1. A resilient business

Diageo is the global leader in alcoholic beverages with an outstanding collection of brands across both spirits and beers.

The brands sold in more than 180 countries include the likes of Johnnie Walker, Crown Royal and Windsor whisky, Smirnoff, Ciroc and Ketel One vodkas, Baileys liqueur and Guinness stout.

It operates in a market that is very large and stable, offering a resilient business against a downturn in the market.

According to Statista, the revenue in the spirits segment will reach US$521.7 billion in 2022 and is expected to grow by 5.3% annually until 2025.

While no company is entirely recession-proof, industries like alcoholic beverages tend to hold up relatively well.

If you keep a stocked liquor cabinet at home, you’re most likely a customer.

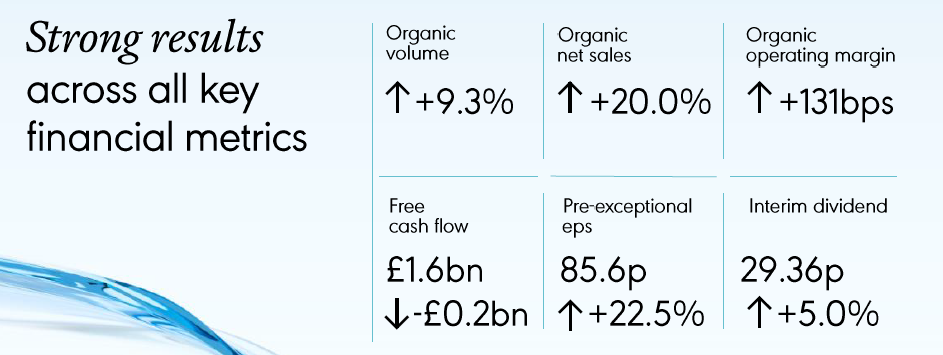

2. Strong results in the first half of fiscal year 2022

Source: Diageo’s Interim Results Fiscal 22, ProsperUs

The UK company recorded an impressive performance in the first half of fiscal year 2022 (1H FY2022).

Net sales were up by 16% (and 20% organically) while reported operating profit increased by 22%, representing an operating margin of 34.5%.

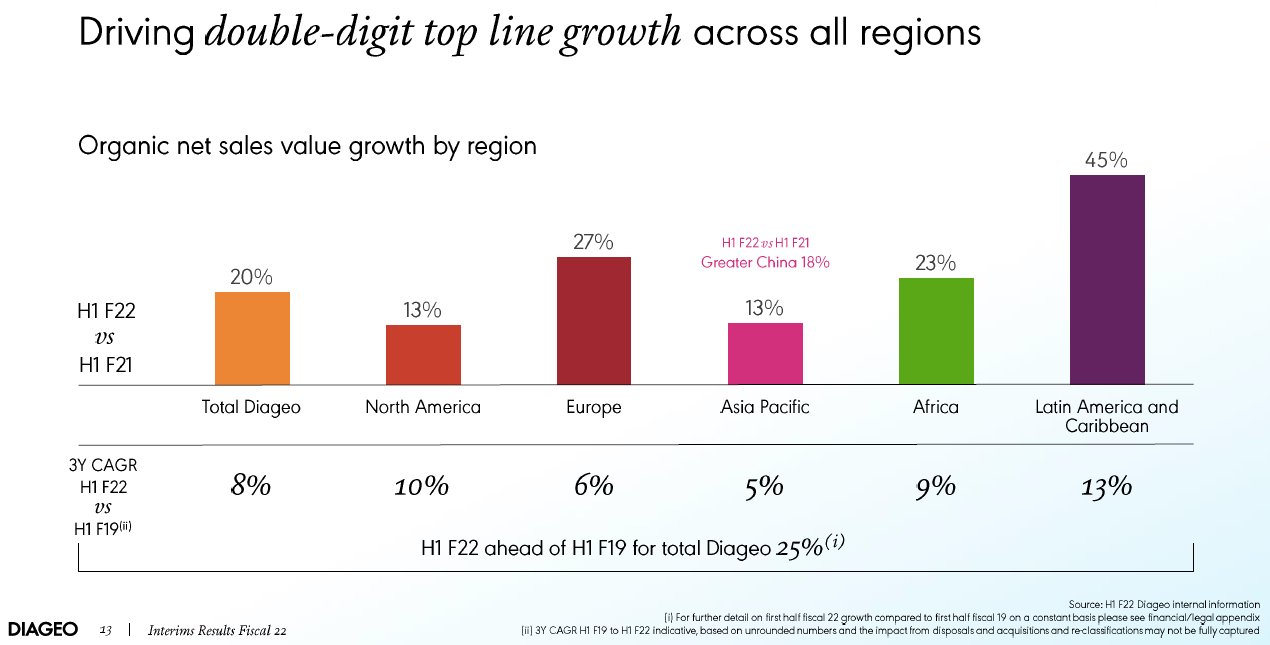

The strong performance was seen across all regions (see below), a reflection of its diversified portfolio across different markets.

Source: Source: Diageo’s Interim Results Fiscal 22, ProsperUs

Source: Source: Diageo’s Interim Results Fiscal 22, ProsperUs

Aside from that, Diageo also reported an increase of 22.5% in its earnings per share (EPS) before exceptional items to 85.6 pence from 69.9 pence.

3. Strong pricing power

In an inflationary environment, it is vital for companies to have a strong pricing power.

Diageo’s gross margin has remained relatively stable at around 60% +/- 2.5% over the last decade.This is mainly due to its strong brand power.

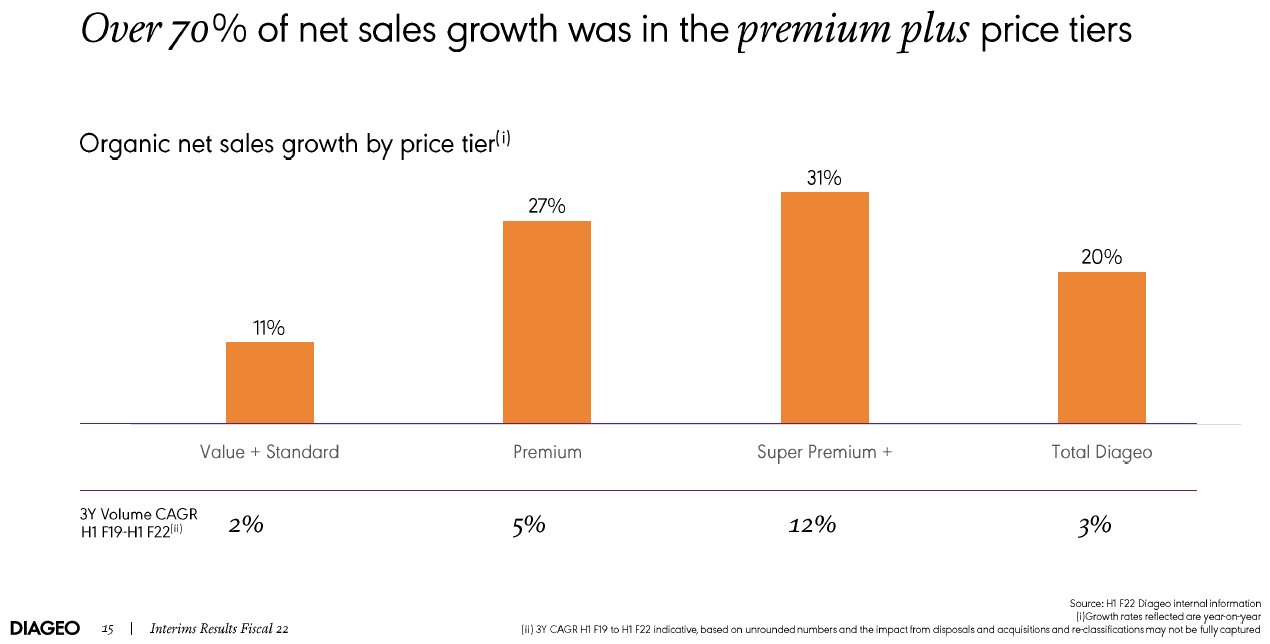

In fact, over 70% of the net sales growth for the company during the 1H FY2022 was in the premium plus price tiers.

Source: Source: Diageo’s Interim Results Fiscal 22, ProsperUs

Source: Source: Diageo’s Interim Results Fiscal 22, ProsperUs

4. Robust balance sheet

The management has shown their ability to manage Diageo’s balance sheet.

The pandemic has caused the company’s leverage to be at 3.5 times its net debt-to-adjusted 12-month earnings before interest, tax, depreciation and amortisation (EBITDA).

By the end of last year, the ratio had improved to 2.5 times, which is the low end of the company’s target range.

As central banks around the world are likely to increase interest rates to combat elevated inflation, a robust balance sheet will ensure the company’s resilience during this time.

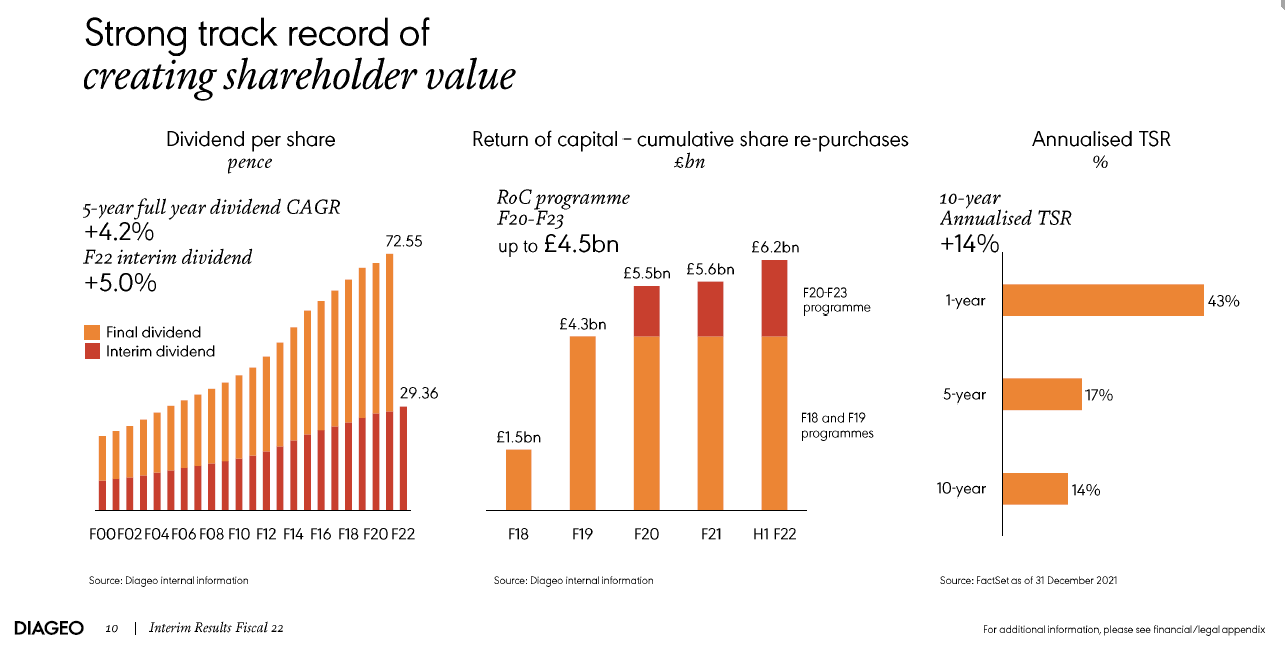

5. Strong dividend track record

Notably, Diageo is a dividend aristocrat as it has grown its dividend over the last 34 years.

In fact, as a sign of confidence in the business, the board of directors approved an increase of the interim dividend of 5% to 29.36 pence per share.

Assuming that the final dividend per share paid in October remains unchanged at currently 44.59 pence, shares of Diageo would currently yield at around 2.0%.

Given the uncertainties in the stock market amid rising inflation and geopolitical tensions, investors will benefit from the safety of its dividend payout – especially in the long-term.

The dividend payout is based on a payout ratio of around 60%, which provides the dividend safety to investors.

Dividend growth of around 4% over the last three years is substantial, especially when we consider the impact of the pandemic on its business earnings temporarily.

Source: Diageo’s Interim Results Fiscal 22, ProsperUs

Source: Diageo’s Interim Results Fiscal 22, ProsperUs

Exceptional company comes at a price

Diageo is a premium company when we look at its valuation. Trading at a trailing price-to-earnings ratio (PE) of 29.3 times, it might seem rather expensive for some investors.

However, through the lens of an income investor, Diageo’s resilient business model and strong dividend track record make it a good company.

It also helps to deflect some of the worries over the volatile market in the near term.

If you’re still uncertain, take a look in your liquor cabinet and it’s probable that you have at least one Diageo brand in there.

With a massive global portfolio of top-ranked brands spanning whisky, beer, vodka, rum, gin and tequila, there’ll always be something for you to toast with when you’re talking about Diageo.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.