Singapore bank stocks have been back in vogue for investors of all stripes recently. And that doesn’t just apply to dividend investors, either.

That’s because the US Federal Reserve (Fed) has been hiking interest rates at its fastest pace in almost four decades.

Clearly, that benefits banks, particularly in a global financial centre like Singapore.

While both UOB reported solid earnings early last week and DBS reported stellar numbers the week before that, there remained only one big bank to report.

Of course, that bank is Oversea-Chinese Banking Corporation Limited (SGX: O39), better known as just OCBC.

OCBC reported its latest H2 2022 and FY2022 earnings last Friday (24 February), before the market opened in Singapore.

With that, here are three quick charts that highlight the big takeaways for Singapore bank investors who are focused on dividends.

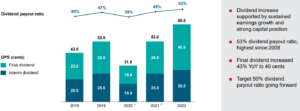

1. Dividend up but no special payout

While there were no surprises on the net interest income (NII) and net interest margin (NIM) fronts, which were both substantially higher, there was some disappointment on OCBC’s dividend.

That’s because, while DBS announced a special dividend payout, OCBC did not. Yet OCBC still raised its final dividend per share (DPS) for FY2022 by nearly 43% year-on-year to 40 Singapore cents.

That was up from FY2021 final DPS of 28 Singapore cents (see below). While the dividend payout ratio for FY2022 was 53%, management stated that it aims for a longer-term payout ratio of 50% going forward.

Source: OCBC H2 2022 and FY2022 earnings presentation

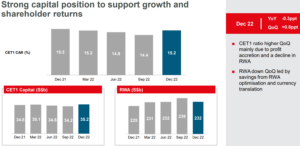

2. CET1 capital ratio supports higher future payouts

However, the good news for OCBC shareholders is that higher future payouts (beyond the 50% number) are not off the table.

That’s because OCBC’s CET1 capital adequacy ratio (CAR) of 15.2% at the end of 2022 (see below) is significantly higher than the 14% CET1 ratio that management is basing its 50% dividend payout policy on.

With lower risk-weighted assets (RWA), estimates are that over S$2 billion in excess capital exists in relation to the CET1 CAR.

That could potentially support a comfortably higher dividend payout while management also didn’t rule out a higher dividend depending on business performance and its capital position.

Source: OCBC’s H2 2022 and FY2022 earnings presentation

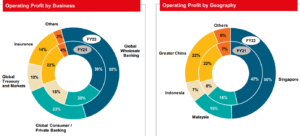

3. Private banking and wealth management could drive 2023 earnings

Then there’s OCBC’s well-renowned wealth management operations. The division actually made up 23% of operating profit in FY2022, versus 20% in FY2021 (see below).

While its fee incomes actually fell in FY2022, the recovery in Greater China – with China and Hong Kong’s reopening – mean that if sentiment stabilises and improves in markets, then this could be a key driver for OCBC in 2023.

Of course, if earnings improve on this front and fee income rises this year on a more buoyant Chinese economy, then a higher dividend payout for shareholders could be forthcoming.

Source: OCBC’s H2 2022 and FY2022 earnings presentation

OCBC dividend yield looks attractive

Overall, it was a quarter which came in slightly below expectations for OCBC given unrealized valuation losses at its insurance subsidiary (Great Eastern).

Yet with a final FY2022 DPS of 68 Singapore cents, OCBC shares are giving investors a 12-month trailing dividend yield of 5.4%.

Of course, if the payout rises this year then the prospective dividend yield (based on today’s price) could come near to 6%. That’s a solid dividend option for Singapore bank investors.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips owns shares of DBS Group Holdings Ltd.