5 Dividend Stocks to Beat Inflation and Rising Interest Rates

November 2, 2022

For investors, 2022 has been an extremely tough year. Stock markets globally have fallen hard, with many of the biggest stocks – particularly in the tech sector – seeing their share prices plummet.

Understandably, investors are unsettled. But one of the best ways to generate positive returns over the long term is to invest in dividend stocks.

The streams of passive income provide support during market volatility and also allows you to reinvest these dividend payments into stocks when their share prices are down.

Otherwise known as the “compounding effect”, this reinvestment process can generate meaningful gains for investors.

As an example, for the S&P 500 Index over the past nine decades (from the 1930s to the 2010s), dividends have made up 41% of the average decade’s total return.

Total return is share price appreciation plus dividends received. Understanding how powerful the compounding of dividends can be means that all investors should have a solid foundation of dividend stocks in their portfolios.

With inflation and rising interest rates battering stocks, it’s also important to identify dividend stocks that grow their dividends faster than the pace of inflation.

So, without any further ado, here are five stocks that can help investors beat inflation and rising interest rates.

1. Home Depot

For those of use who own their own property, you’ll know that it requires constant maintenance. Well, in the US (and North America generally), home improvement retail is a multi-billion-dollar business.

That’s where Home Depot Inc (NYSE: HD) comes in. The leading home improvement retail chain globally, the company has over 2,300 stores across the US, Canada, and Mexico.

Home Depot employs over 500,000 people and a typical store averages around 105,000 square feet in space – offering both DIYers and professional contractors with a comprehensive range of choice for their needs.

Last year, the company racked up over US$150 billion in sales for the full year 2021. What’s more, its return on invested capital (ROIC) is extraordinary – coming in at 44.7% in 2021 versus 40.8% in 2020.

As for so far in 2022, the housing market has understandably slowed in the US. However, consumers are still spending on sprucing up their homes.

That’s come through in Home Depot’s earnings. In its Q2 FY2022, the company reported revenue of US$43.8 billion, up 6.5% from the same period in 2021.

More importantly, the company reaffirmed in fiscal 2022 guidance. Primarily this forecasts its diluted earnings per share (EPS) growing by mid-single digits.

The company’s massive cash flow, both on the operating and free cash levels, allows Home Depot to pay a handsome dividend.

Over the past 20 years, Home Depot has hiked its dividend at a compound annual growth rate (CAGR) of 19.7%.

While its shares currently yield only 2.6%, the track record length and – crucially – growth rate of the dividend means Home Depot is a dividend star.

2. Mapletree Industrial Trust

Second is a large real estate investment trust (REIT) that’s listed in Singapore, Mapletree Industrial Trust (SGX: ME8U).

The big industrial and data centre REIT has 141 properties across both Singapore and North America, with assets under management of S$8.9 billion as of 30 September 2022.

Just over 50% of its AUM is concentrated in North American data centres while the remaining 49% or so is in Singapore – split among flatted factories, light industrial buildings, data centres, business park buildings, and hi-tech buildings.

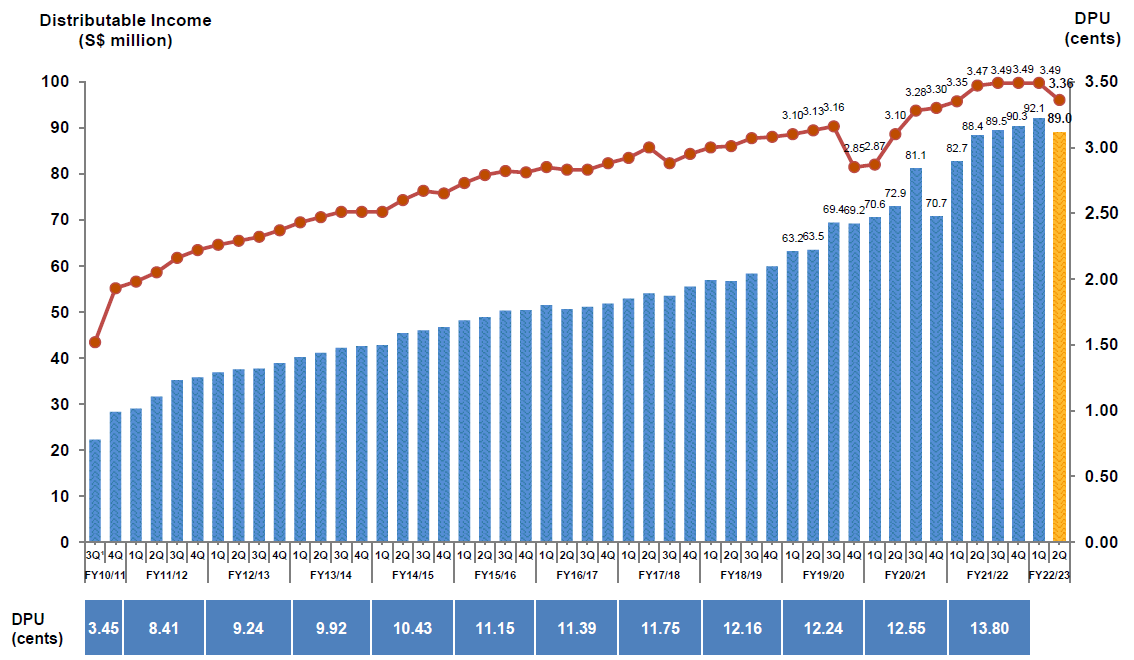

The REIT has one of the best track records of any Singapore REIT over the past decade or so, both in terms of growing its distribution per unit (DPU) and its share price performance.

While Mapletree Industrial has been impacted by rising interest rates, it has managed to grow its DPU (or dividend) by a CAGR of 5.1% over its past 10 full fiscal years (FY2012-FY2022).

However, with rising interest rates expected to be a headwind for REITs going forward, its DPU could be negatively affected.

That doesn’t mean that the REIT’s assets won’t continue to produce higher income though.

In fact, in its latest earnings update, Mapletree Industrial saw its average portfolio occupancy increase while it also witnessed positive rental reversion for its Singapore portfolio.

While it did see its DPU slip year-on-year, it still boasts an extremely impressive track record in terms of growing its DPU and distributable income (see below).

At its current price of S$2.20, Mapletree Industrial Trust offers investors a 12-month forward dividend yield of 6.1%.

Source: Mapletree Industrial Trust Q2 FY2022/2023 earnings presentation

3. NextEra Energy Partners

Clean, or renewable energy, is a massive business. And it’s only going to get bigger. That’s why NextEra Energy Partners LP (NYSE: NEP) is such a compelling dividend stock.

The company owns and operates a big chunk of clean energy assets – including wind, solar and battery storage – with total generation capacity of 8 gigawatts (GW).

Its parent firm is renewable energy behemoth NextEra Energy Inc (NYSE: NEE).

Essentially, with its parent’s large portfolio of renewable energy-generating capacity, NextEra Energy Partners is able to purchase clean energy assets while also steadily increasing its cash available for distribution (CAFD) over time.

This has resulted in some extraordinary growth in its dividend over the long term.

While NextEra Energy partners operates a yieldco – and only went public in 2014 – it has managed to grow its dividend by over 320% since then.

Not only that, the company raises its dividend every quarter, something which it has done ever since listing.

That has allowed its distribution to expand at a CAGR of 18.6% over the past seven years (2015-2022).

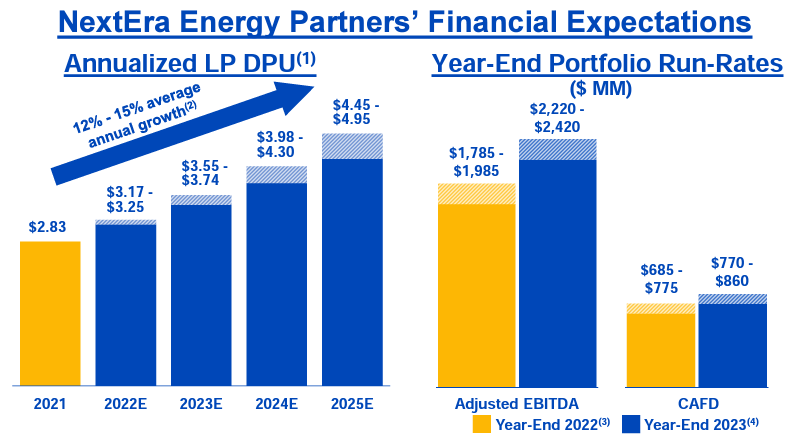

What’s more, management is confident in predicting that it can meet projections for 12-15% average annualised growth in its distribution per unit (DPU) through 2025 (see below).

With an annualised DPU of US$3.15, NextEra Energy partners shares offer investors a dividend yield of 4.2%.

Source: NextEra Energy Partners Q3 2022 earnings presentation

Source: NextEra Energy Partners Q3 2022 earnings presentation

4. DBS Group

While REITs may not benefit from rising interest rates, banks do. That’s why DBS Group Holdings Ltd (SGX: D05) is such a solid dividend stock for long-term investors.

Singapore’s biggest bank has a robust track record of growing its dividend as well as earnings.

After going through over a decade of near-zero interest rates, banks are finally benefitting from higher rates through elevated net interest margin (NIM) and net interest income (NII).

All of Singapore’s banks are seeing both higher NIM and NII as the US Federal Reserve continues to hike rates aggressively.

Effectively, how banks benefit from this is that they can earn more between the interest rate they pay savers (those of us with current and savings accounts – also known as “CASAs”) and the interest rate they charge for loans.

This spread has been widening as the cost of capital has become more expensive, meanings loans (such as mortgages) start to become pricier.

Along with a solid acquisition strategy and improvements in its technology stack, DBS has seen its share price perform well since the Covid-19 lows.

Finally, its impressive earnings profile and above-average return on equity (ROE), which came in at 13.4% in Q2 2022, mean the bank has been able to grow its dividend.

Over the past decade, DBS has grown its dividend per share (DPS) at a CAGR of 9.9%. Currently, DBS shares are offering investors a dividend yield of 4.2%.

5. Accenture

Last but not least is global powerhouse technology consultant Accenture Plc (NYSE: ACN).

The consultant is the leading brand for companies looking to improve their processes and operations. Consulting is also a highly-lucrative business with a steady stream of demand.

In its FY2022 (for the 12 months ending 31 August 2022), Accenture posted record revenue of US$61.6 billion, a 26% year-on-year increase in local currency terms.

Its growth profile was also pretty evenly-split across its geographic markets with all regions seeing strong increases; North America was up 23% year-on-year (to US$29.1 billion), Europe was up 29% year-on-year (to US$20.3 billion), and Growth Markets was up 29% year-on-year (to US$12.2 billion).

Meanwhile, earnings per share (EPS) came in at US$10.71, up 22% year-on-year on an adjusted basis.

Fittingly, the company is returning its massive free cash flow to shareholders in the form of dividends and share buybacks.

In FY2022, Accenture saw record high free cash flow of US$8.8 billion. It paid out US$2.5 billion in dividends while buying back US$4.1 billion worth of shares.

I’d like to see more of that free cash flow go towards growing the dividend but you can’t complain with the growth rate.

Over the past decade, Accenture has hiked its dividend at a CAGR of 11.1%. That easily beats the rate of inflation – even in today’s volatile environment.

Currently, Accenture shares give investors a 12-month forward dividend yield of 1.6%.

Mix higher yielders with growers

For dividend investors, it’s smart to have a mix of both solid dividend stocks that provide a higher yield, along with lower-yielding stocks that can grow their dividends at a fast rate.

That way, long-term investors are diversified across the dividend spectrum and have exposure to all types of dividend stocks.

With Home Depot, Mapletree Industrial Trust, NextEra Energy Partners, DBS Group, and Accenture, long-term investors have five great stocks that can beat inflation amid a rising interest rate environment.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips owns shares of Home Depot Inc, Mapletree Industrial Trust, NextEra Energy Partners LP, DBS Group Holdings Ltd and Accenture Plc.

Tim Phillips

Tim, based in Singapore but from Hong Kong, caught the investing bug as a teenager and is a passionate advocate of responsible long-term investing as a great way to build wealth.

He has worked in various content roles at Schroders and the Motley Fool, with a focus on Asian stocks, but believes in buying great businesses – wherever they may be. He is also a certified SGX Academy Trainer.

In his spare time, Tim enjoys running after his two young sons, playing football and practicing yoga.