It’s that time of year again; earnings season. As is customary, many of Singapore’s biggest REITs are the earliest companies to report their quarterly numbers in Singapore.

Just yesterday, after the market closed, Mapletree Logistics Trust (SGX: M44U) reported its latest Q3 FY22/23 earnings (for the three months ending 31 December 2022).

The pan-Asian logistics REIT owns over 180 properties across multiple countries in Asia and is also a constituent member of the Straits Times Index (STI).

So, for dividend investors and S-REIT lovers, here are eight key takeaways from Mapletree Logistics Trust’s latest results.

1. Revenue and net property income increase

For Mapletree Logistics Trust, both its gross revenue and net property income (NPI) rose on a year-on-year basis.

Gross revenue was up 8.0% year-on-year to S$180.2 million while NPI increased by 7.3% year-on-year to S$157.2 million.

Revenue growth contributions came from accretive acquisitions completed in Q1 FY22/23 and FY21/22.

However, on a quarter-on-quarter basis, the REIT’s revenue was down 2% and NPI was down 1.8%.

2. DPU up on year…but down on quarter

For all dividend investors, a REIT’s distribution per unit (DPU) is key as it measures the amount of money you’ll get for every unit you hold.

In Mapletree Logistics Trust’s Q3 FY22/23, its DPU was up 1.9% year-on-year to 2.227 Singapore cents. However, this figure was down on a quarter-on-quarter basis by 0.9%.

That was mainly attributed to exchange rate fluctuations and the weakness of other Asian currencies versus the Singapore dollar.

3. Borrowing costs soar

During the quarter, Mapletree Logistics Trust’s borrowing costs hit S$34.8 million, soaring by 36.2% when compared to the same period a year earlier.

Clearly, rising interest rates have had an impact on the REIT’s borrowing costs while incremental borrowings to fund acquisitions also added to costs.

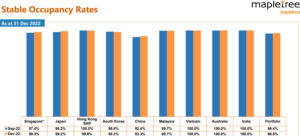

4. Portfolio occupancy climbs

Overall, it was a stable showing from the REIT in terms of its portfolio. That’s because occupancy rates, as of the end of December 2022, actually climbed to 96.9%.

This was up from 96.4% occupancy for its overall portfolio as of the end of September 2022.

As readers can see below, a lot of this was driven by higher occupancy rates in Singapore, Japan, and China.

Source: Mapletree Logistics Trust Q3 FY22/23 earnings presentation

5. Over 80% of debt on fixed rates

Thankfully for unitholders, the REIT has been responsible with ensuring a lot of its debt load in on fixed rates.

As of 31 December 2022, 83% of its total debt – of S$4.9 billion – was hedged or drawn in fixed rates.

Meanwhile, around 79% of the amount distributable over the next 12 months has been hedged into, or is derived in, Singapore dollars.

6. Gearing ratio rises slightly

For any REIT, the leverage ratio is important and in Mapletree Logistics Trust’s case, its gearing ratio is 37.4%.

That’s comfortably under the 50% MAS-imposed cap but it’s also slightly higher than the 37.0% gearing ratio it had at the end of September 2022.

7. Weighted average annualised interest rate increases

Higher interest rates have impacted all Singapore REITs. For Mapletree Logistics Trust, its weighted average annualised interest rate – as of 31 December 2022 – was 2.6%.

While still relatively low versus peers, it was up 10 basis points (bps) from the 2.5% weighted average annualised interest rate it recorded at the end of September 2022.

8. Divestments on track

The logistics REIT has announced over the past month that it would be divesting three properties; one in Singapore (at 3 Changi South) and two in Malaysia.

These divestments are set to help Mapletree Logistics Trust redeploy capital towards investments in more modern facilities with better specs.

All properties were sold at a premium to to independent valuation. The Singapore property divestment is on track to be completed in Q4 FY22/23 while the sale of the Malaysia properties will completed in H1 FY23/24.

Stable showing from key STI REIT

There were no real surprises in the latest quarterly earnings from Mapletree Logistics Trust. It was another solid showing in what’s a challenging operating environment.

Management did note in the release that it would continue to focus on cost management and value-add opportunities via asset enhancements and divestments, while also looking at growth opportunities to strengthen its portfolio.

The REIT’s distribution (or dividend) will be paid out to shareholders on 13 March, 2023. The record date, to be eligible for the distribution, will be 31 January 2023.

As its current price, Mapletree Logistics Trust is offering investors a 12-month forward dividend yield of 5.4%.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips owns shares of Mapletree Logistics Trust.