Shopping mall operator Frasers Centrepoint Trust (SGX: J69U), which owns a portfolio that comprises of nine suburban retail malls and one office building, reported a strong business update for its fiscal first quarter ended 31 December 2022 (Q1 FY2023).

Frasers Centrepoint Trust, or FCT for short, owns retail malls that are situated near Singapore’s MRT stations or bus exchanges as well as populous residential areas.

Among some of these retail malls include the likes of Causeway Point, Waterway Point, Tampines 1, Tiong Bahru Plaza, Century Square, Changi City Point, and others.

This allows FCT to enjoy high shopper traffic comprised of residents and commuters.

During the business update for Q1 FY2023, there were signs that the ongoing retail recovery in Singapore has now surpassed pre-COVID levels and that this trend will continue with the support of the return of Chinese tourists.

For Singapore REIT investors, here are some of the key highlights from FCT’s business update for Q1 FY2023.

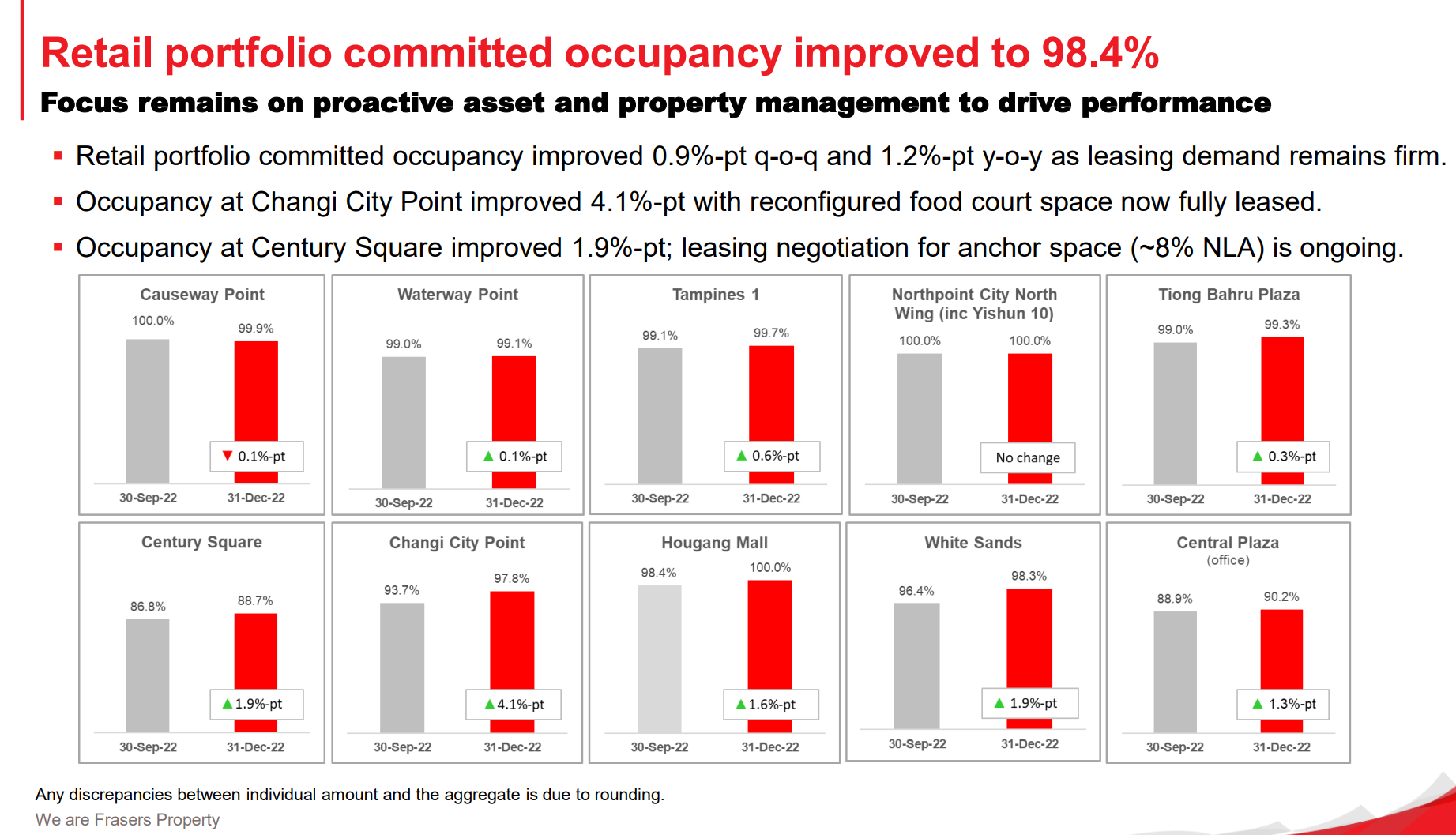

Retail portfolio occupancy shows strong improvement

FCT’s portfolio committed occupancy improved 0.9 percentage points (ppts) on a quarter-on-quarter (qoq) and 1.2 ppts on a year-on-year (yoy) basis to 98.4%.

The improvement came mainly from the 4.1 ppts qoq increase in Changi City Point, 1.9 ppts qoq increase in Century Square and White Sands and 1.6 ppts qoq increase in Hougang Mall.

In Changi City Point, the reconfigured food court space has now been fully leased while leasing negotiations for anchor space in Century Square are still ongoing.

Source: FCT’s Q1 FY2023 Business Updates

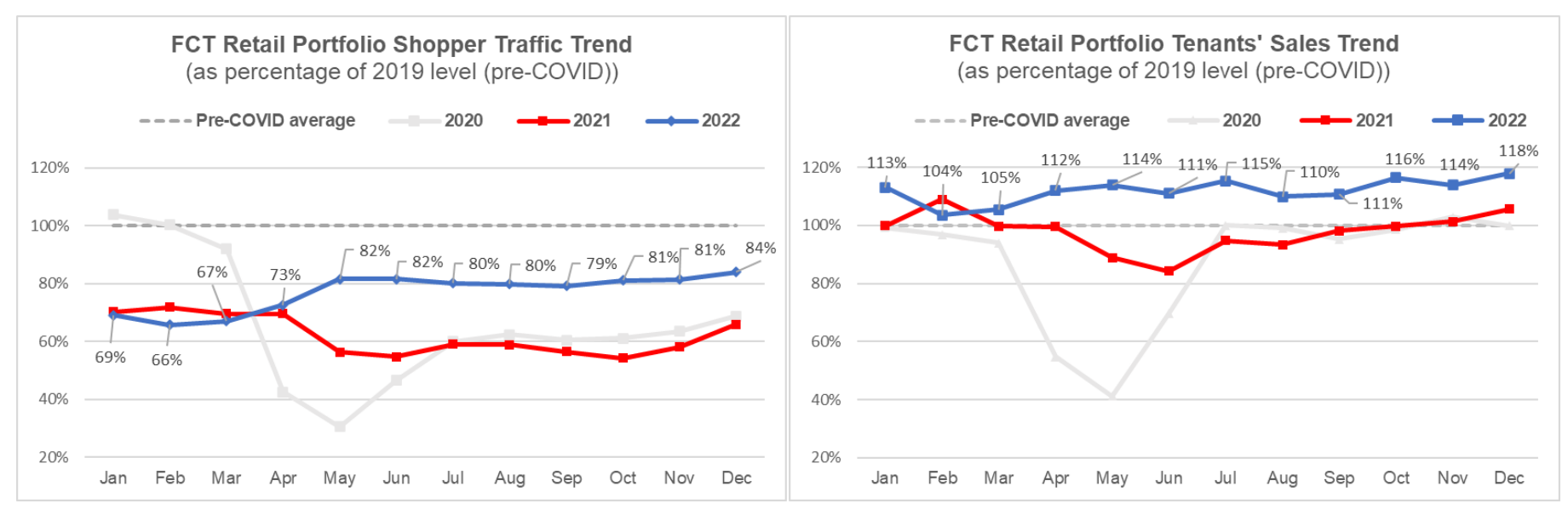

Retail sales surpassed pre-COVID levels despite lower shopper traffic

One of the key highlights in the business update is that mall visitations have become more purposeful.

This is seen by the increase in tenant sales above pre-COVID level (by 12%) despite shopper traffic that averaged at around 80% of pre-COVID levels in 2022.

Source: FCT’s Q1 FY2023 Business Updates

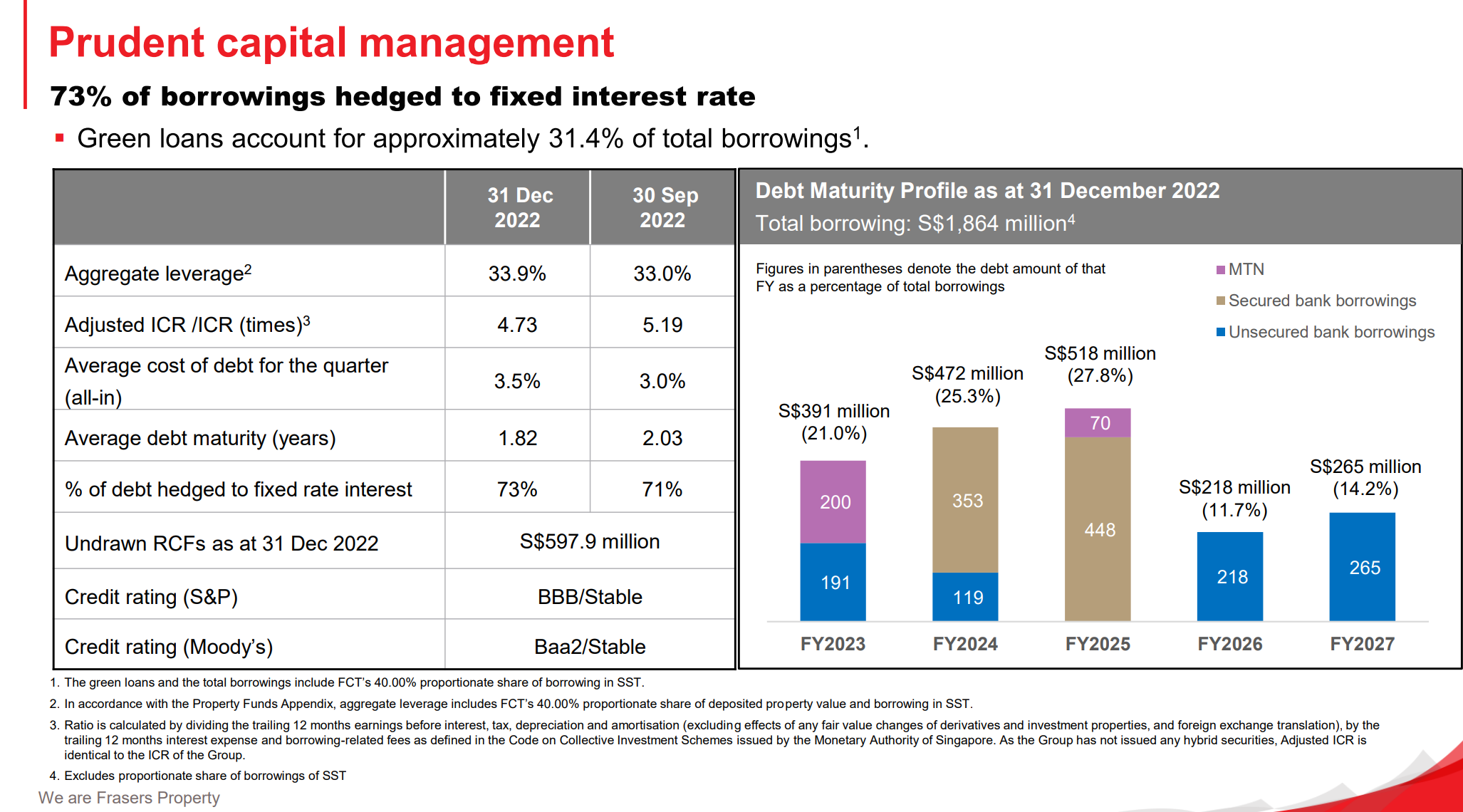

Solid debt profile despite increasing cost

The rising interest rate environment has led to an increase in the cost of debt and FCT has not been spared from this trend.

In Q1 FY2023, the REIT’s average cost of debt increased to 3.5% as compared to the 3.0% in the previous quarter.

Despite that, FCT has a solid debt profile with a gearing ratio of only 33.9%.

Meanwhile, 73% of its total borrowings are also hedged to fixed interest rates as compared to just 71% in the previous quarter.

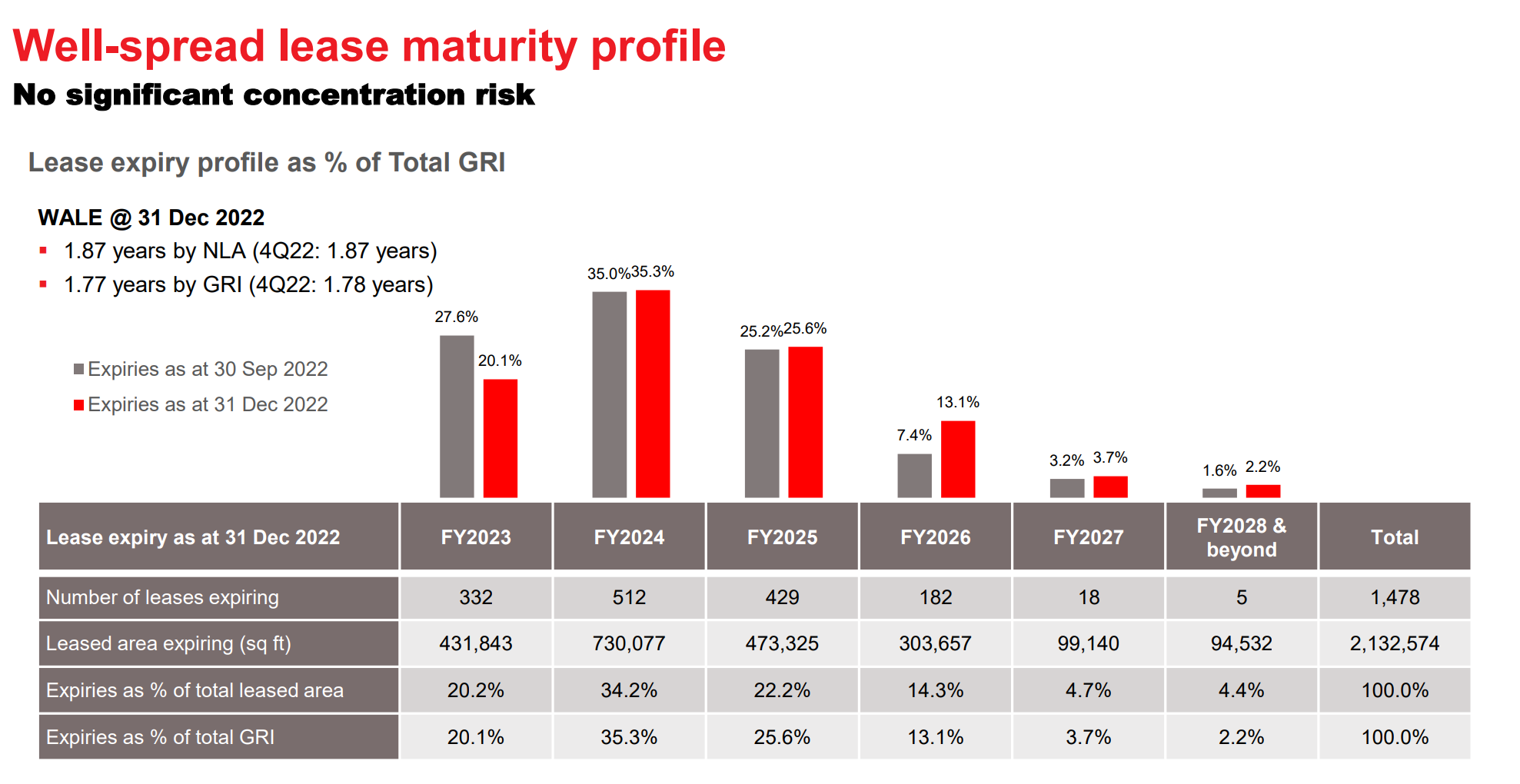

Another key highlight is the lease expiry profile of FCT, which has around 20.2% of its leases expiring in FY2023.

As a retail REIT, FCT has a relatively shorter weighted average lease expiry (WALE) of 1.87 years, by net lettable area (NLA).

I think this bodes well for FCT since the inflationary environment and strong leasing demand should support positive rental reversions, which would help offset rising costs.

Source: FCT’s Q1 FY2023 Business Updates

Asset enhancement initiatives in Tampines 1

Investors should also take note of FCT’s asset enhancement initiatives (AEI) at Tampines 1 that will add an additional 8,000 sq ft of NLA.

It will cost around S$38 million in rejuvenation and enhancement capital expenditure for FCT.

Prior to the commencement of the AEI works, there was over 70% pre-commitment for AEI spaces while value generation from higher rents, asset valuation gains and sustainable asset performance is expected to drive a return on investment (ROI) of 8%.

The AEI will commence in phases from Q2 FY2023 and is expected to be completed by Q3 FY2024 with the malls to continue in operation during the AEI period.

A Singapore REIT that focuses on retail recovery

FCT had a strong recovery since falling into its one-year low of S$1.92 in November last year.

In fact, the REIT’s share price has increased by 8.4% since Tim wrote an article on FCT back in November last year during its H2 FY2022 earnings.

What is clear from the business update in Q1 FY2023 is that the strong retail recovery in Singapore has continued.

Additionally, with the return of Chinese tourists, I believe FCT is in a good position to maintain its solid performance despite rising costs.

For Singapore investors, the REIT is a solid way of gaining exposure to the continued recovery of the Singapore consumer as the economy reopens and benefits accordingly.

FCT also offers an attractive forward dividend yield of 5.6% to investors looking to build their wealth through dividend investing.

With the return of Chinese tourists, I believe that FCT’s malls will see shopper traffic return to pre-COVID levels, further supporting growth for the retail-focused REIT in Singapore.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.