For long-term investors, the short-term stock market reactions to quarterly earnings can provide us with two things; a useful look at the state of the business and a potential buying opportunity.

That’s particularly true for stocks we intend to hold long term. So, in Singapore, dividend investors who want to buy the best income-generating REITs are getting a good view of how they’re doing coming out of Covid-19.

Recently, one of Singapore’s biggest REITs, Mapletree Logistics Trust (SGX: M44U), reported its Q2 FY 2021/2022 earnings (for the three months ended 30 September 2021).

It was a solid report for the logistics REIT that is backed by large Singaporean investment firm Mapletree Investments Pte Ltd.

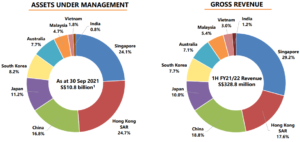

Owning 163 properties across Singapore, Hong Kong, China, Japan, South Korea, Australia, Malaysia, India, and Vietnam, Mapletree Logistics Trust is a truly regional logistics REIT.

With investors focused on finding dividend-paying stocks that can sustainably keep paying shareholders, is Mapletree Logistics Trust still a buy?

Diversified and growing

For its most recent fiscal second-quarter 21/22 results, Mapletree Logistics Trust saw net property income (NPI) rise 21.5% year-on-year to S$144.4 million.

Meanwhile, the all-important distribution per unit (DPU) rose by 5.7% year-on-year to 2.173 Singapore cents.

The slower pace of DPU growth relative to the NPI expansion reflects the enlarged unit base due to an equity fund raising carried out earlier this year.

However, with its DPU hitting an all-time high, it remains on track to keep growing its logistics footprint in Asia.

Even better for investors, Mapletree Logistics Trust’s diversification across countries is one of its key strengths.

During its latest quarter, no one country made up more than 30% of the REIT’s gross revenue (see below).

Source: Mapletree Logistics Trust Q2 FY21/22 earnings presentation

Plans are also afoot for the REIT to keep adding properties to its sizeable portfolio. In mid-August Mapletree Logistics announced it would be buying an Australian logistics property for S$42.8 million.

Just last week, it also announced a plan to purchase a modern logistics facility in South Korea for S$153.8 million.

Acquisitions to ramp up

During the quarterly earnings call, Mapletree Logistics management did say it expects to close a deal in Japan in the coming month and acquire more properties in China and Vietnam over the next six months.

With a focus on broadening out its asset base, through attractive DPU-accretive acquisitions in North Asia, Mapletree Logistics is clearly leading the way as an Asian logistics property player.

Trading at around S2.01 per unit, and offering investors a relatively decent 12-month forward dividend yield of 4.3%, Mapletree Logistics Trust should continue to benefit from the rising penetration of e-commerce in Asia.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips owns shares of Mapletree Logistics Trust.