In times of uncertainty, such as now, long-term investors should be thankful for the “rock-steady” parts of their portfolios.

These tend include stocks that generate passive income and pay a dividend. Among them are Singapore’s real estate investment trusts (REITs).

That’s because, as higher inflation eats away at our cash, there’s actually good reason to buy and hold Singapore REITs.

A slew of REITs reported earnings last week and this week. One constituent stock of the Straits Times Index (STI), and one of Singapore’s biggest REITs, is industrial and data centre property owner Mapletree Industrial Trust (SGX: ME8U).

The REIT reported its fourth-quarter fiscal year (FY) 21/22 earnings (for the three months ending 31 March 2022) this past Tuesday.

So, were investors impressed with the industrial REIT’s latest earnings and how should dividend investors view its prospects going forward?

Full-year dividend up 10%

For dividend invetsors who rely on consistent income streams, the one number they should care about is the distribution per unit (DPU), and whether that is growing consistently.

Thankfully for shareholders in Mapletree Industrial Trust, its DPU for the whole of FY21/22 was up 10% year-on-year to 13.80 Singapore cents.

For the most recent quarter, the REIT’s DPU rose 5.8% year-on-year to 3.49 Singapore cents. While this was flat quarter-on-quarter, it came in ahead of expectations.

Meanwhile, on the portfolio occupancy side, there was positive news. Mapletree Industrial Trust’s portfolio occupancy in Q4 FY21/22 improved to 94.0%, from 93.6% in the prior quarter.

This was mainly from the Singapore part of its portfolio, where the occupancy rate increased to 94.4% in its most recent quarter from 93.7% in the prior quarter.

Average Singapore rents were broadly stable for the quarter but the REIT did say that its rent arrears were slightly lower at 0.8% of the trailing 12 months’ gross revenue, compared to 1.0% as of 31 December 2021.

Stable financial metrics

The most recent quarter was relatively in line with its reputation for financial discipline. The REIT’s weighted average all-in funding cost for the quarter was only 2.4%, up only 10 basis points from 2.3% as of 31 December 2021.

While its interest coverage ratio (ICR) came down to 5.7x as of 31 March 2022, from 6.4x as of the end of 2021, it’s still a robust coverage ratio.

Meanwhile, its gearing ratio fell to 38.4% in its latest quarter, from 39.9% at the end of last year, given the take-up rate of its distribution reinvestment plan (DRP) for Q3 FY21/22’s payout was at a healthy 42.5%.

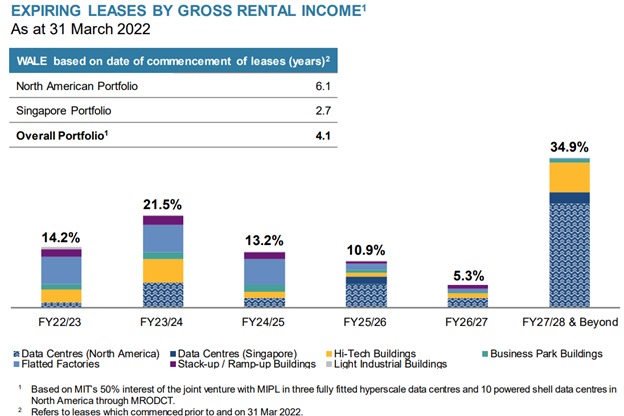

Its lease expiry profile looks manageable this fiscal year and next (see below), with just over one-third of its total leases up for renewal.

Source: Mapletree Industrial Trust Q4 FY21/22 earnings presentation

Costs need to be monitored

At the end of the day, investors in Mapletree Industrial Trust can be content with another reliable quarter from the REIT.

Its portfolio value increased 28.9% year-on-year over FY21/22 to a record S$8.7 billion as new acquisitions added value and fed through into its increased DPU.

Meanwhile, management reiterated its medium-term goal of raising the its data centre exposure (in terms of AUM) to two-thirds from its most recent 54%.

One thing investors should watch, though, is the rising cost of electricity as higher utilities cost could impact its margins in the short term.

Management did note that utilities contracts would be gradually renewed as we enter the halfway point of 2022.

Yet, trading at a 12-month forward dividend yield of 5.3%, Mapletree Industrial Trust is currently offering long-term investors a chance to buy into quality assets at an attractive yield.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips owns shares of Mapletree Industrial Trust.