One of the two largest investment banks in the world, Goldman Sachs Group Inc (NYSE: GS), saw a decline of 6.4% in its share price after the bank reported its worst earnings miss in a decade for the fourth quarter of 2022.

Quarterly profit plunged 66% from a year earlier to US$1.33 billion, or US$3.32 per share, while revenue was down 16% to US$10.59 billion during the same period.

The reported earnings were about 39% below the consensus estimate of US$5.48 per share (based on Refinitiv survey data) while revenue was just below the consensus estimate of US$10.83 billion.

Here are some of the reasons for Goldman Sachs’ underperformance during the quarter.

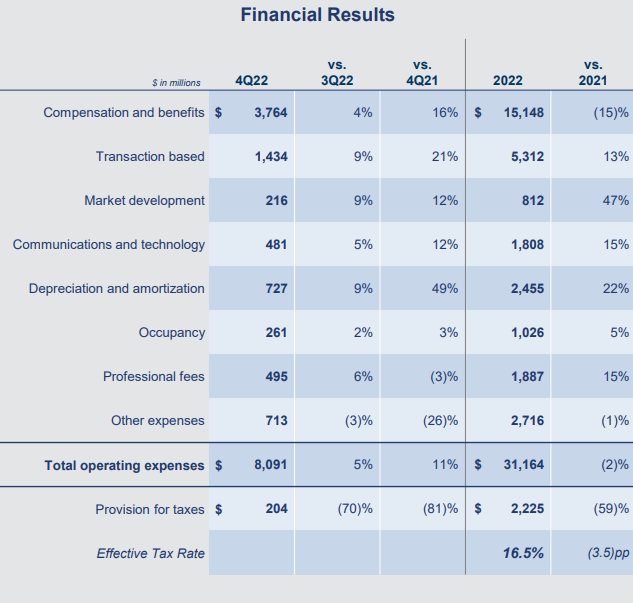

1. Operating expenses shot up by 11%

One of the main reasons for the underperformance during the quarter was due to higher operating expenses, which have increased by 11% year-on-year.

The sharp increase was mainly due to the 16% increase in compensation and benefits, as well as transaction-based fees.

It is also worth noting that client-driven market development costs were higher following low levels during the pandemic.

Source: Goldman Sachs’ Q4 FY2022 Presentation

Despite the sharp increase in compensation and benefits costs during the quarter, compensation expenses were actually down by 15% for the full year 2022 as compared to a year ago.

Meanwhile, total operating expenses were also lower by 2% in 2022.

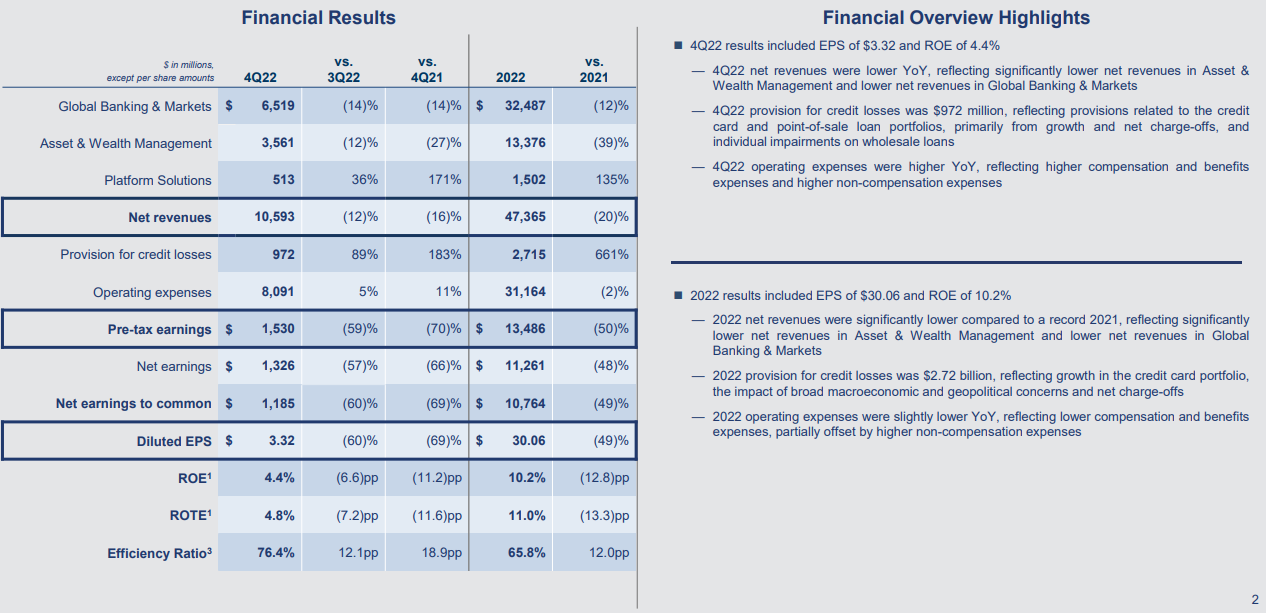

2. Higher provision of credit losses in Q4 2022

Source: Goldman Sachs’ Q4 FY2022 Presentation

Another reason for the big earnings miss was the different expectations of analysts and management on the health of consumer credit.

In Q4, Goldman Sachs’ provisions for credit losses increased by 183% to S$972 million from a year ago as the bank set aside more funds for potential losses in credit card and point-of-sale loan portfolios.

Denis Coleman, the CFO of Goldman Sachs, said this during its earnings call with analysts:

“Our provision for credit losses was $972 million. For our wholesale portfolio, provisions were driven by impairments and portfolio growth. The overall credit quality of our wholesale lending portfolio remains resilient.

In relation to our retail portfolio, provisions were driven by continued portfolio growth, net charge-offs and a worsening of our baseline scenario.

We are seeing early signs of credit deterioration that are in line with our expectations. We anticipate further pressure in 2023 given the vintage and nature of our portfolio.”

3. Sharp decline in investment banking fees

The decline in Goldman Sachs’ top line was mainly due to the lower results from its key business division, Global Banking & Markets, as well as from Asset & Wealth Management.

The Global Banking & Markets division revenue was down by 14% while asset & wealth management’s revenue was lower by 27% from a year ago.

Under Global Banking & Markets, the lower revenue was due to the 48% decline in investment banking fees, to US$1.87 billion, on muted issuance activity in equity and debt markets and lower advisory fees.

Meanwhile, Asset & Wealth Management’s performance was weaker due to a far smaller gains on private equity holdings and markdowns in debt instruments.

Doing too much, too quickly

Goldman Sachs has already laid off 3,200 employees last week as the Group acknowledged some of the missteps in the 153-year-old investment bank’s aim to become a major player in US consumer banking.

With issues such as product delays, executive turnover, branding confusion, regulatory missteps and deepening financial losses, Goldman Sachs will scale down its consumer operations ambitions.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.