Investors have been eagerly awaiting earnings reports from the three leading local banks in Singapore.

That’s because they want to evaluate the economy’s performance amid considerable uncertainty, heightened by increasing interest rates and ongoing inflationary pressures over the past year.

This is as Singapore banks serve as a mirror to the real economy as they extend loans to a broad range of people and businesses.

So, United Overseas Bank Ltd (SGX: U11), or UOB, was the first among the three Singapore banks to share its financial results for the first quarter of 2023 (Q1 FY2023).

While UOB has not failed to impress with its solid results, I believe it will be difficult to sustain the earnings growth momentum going forward.

Here are three key highlights from UOB’s numbers for investors who own any of the Singapore banks.

1. Stellar earnings but slower loan growth

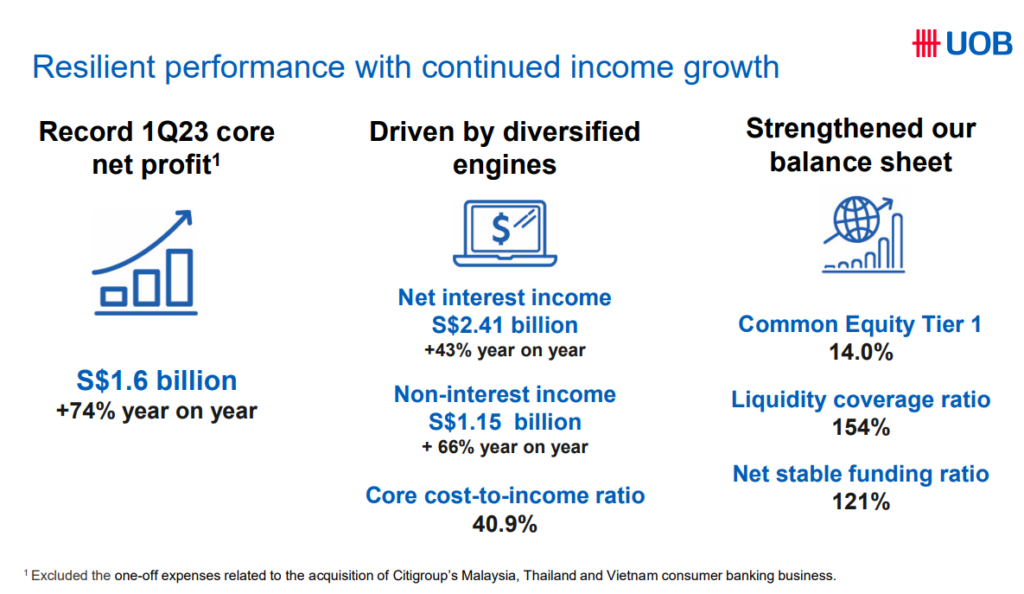

Source: UOB’s Q1 FY2023 CEO Presentation

UOB’s financial performance for Q1 FY2023 aligned with expectations, as core net profit surged by 74% year-on-year (YoY) and 13% quarter-on-quarter (QoQ) to S$1.6 billion.

Net profit, inclusive of one-time expenses related to the acquisition of Citibank’s retail assets in Malaysia and Thailand in November 2022, experienced a growth of 67% YoY and 31% QoQ, reaching S$1.51 billion.

These record earnings were primarily driven by a substantial uptick in both net interest income (NII) and non-interest income, which expanded by 43% YoY and 66% YoY, respectively.

The rebound in wealth management fees and reinforced trading and investment fees contributed to the non-interest income surge, owing to enhanced investor sentiment and proactive trading and liquidity management activities.

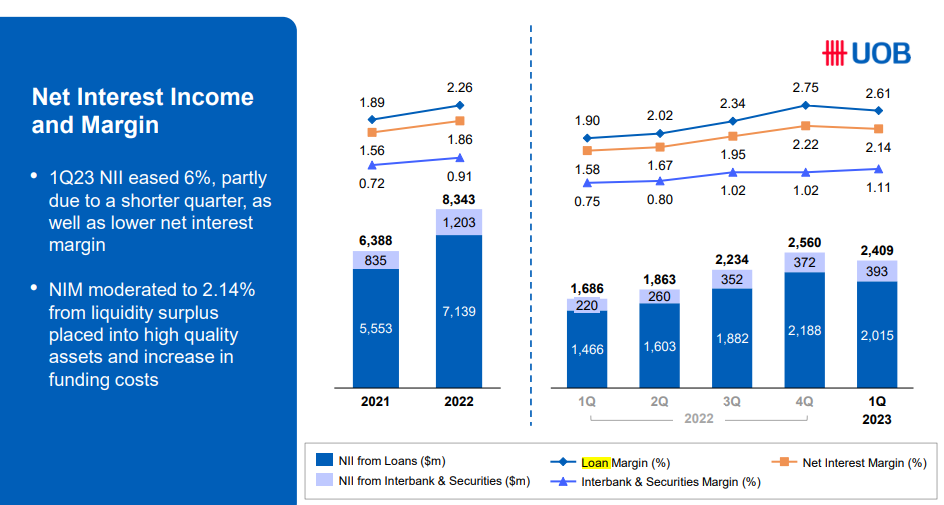

Source: UOB’s Q1 FY2023 Financial Updates

Over the quarter, the net interest margin (NIM) widened by 56 basis points (bps) compared to the previous year, although it contracted by 8bps QoQ to settle at 2.14%.

This expansion contributed to a 43% YoY increase in NII, totalling S$2.41 billion, albeit with a 6% decline from the prior quarter.

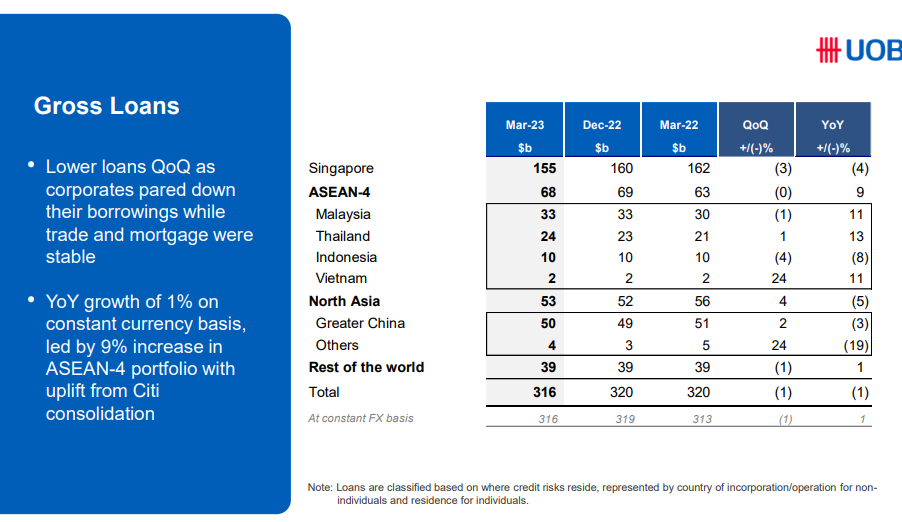

Source: UOB’s Q1 FY2023 Financial Updates

Despite a 1% QoQ decrease in loan growth due to reduced corporate borrowing, trade and mortgage loans remained stable.

Factoring in constant currency and Citibank’s consolidation, gross loans experienced a 1% YoY growth, bolstered by a 9% increase in the ASEAN-4 portfolio.

2. Effective cost management and stable NPL

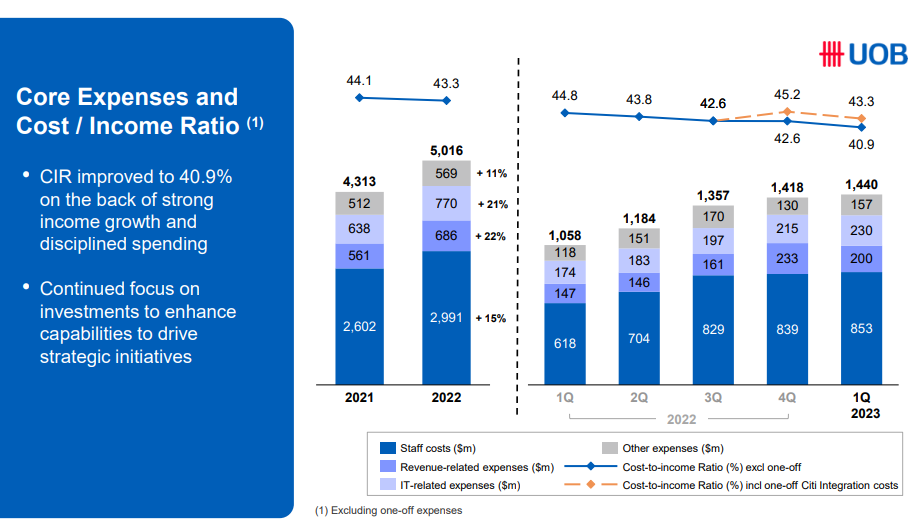

UOB’s cost-to-income ratio (CIR) improved to 40.9% for Q1 FY2023 amid strong income growth and disciplined spending.

This figure is notably lower than the 44.8% recorded in Q1 2022 and 42.6% in the previous quarter (Q4 2022).

Asset quality demonstrated resilience as the non-performing loans (NPL) ratio persisted at a stable 1.6%. Credit cost was higher at 25bps with pre-emptive general allowance allocation.

Aside from that, the current account and savings account CASA ratio improved to 47.9% in Q1 FY2023 from 47.5% in Q4 FY2022, which is an encouraging signal that points to stabilising funding cost.

The bank’s balance sheet remains strong, boasting a common equity tier-1 (CET1) ratio of around 14%, reflecting an enhancement of 0.7 percentage points QoQ and 0.9 percentage points YoY.

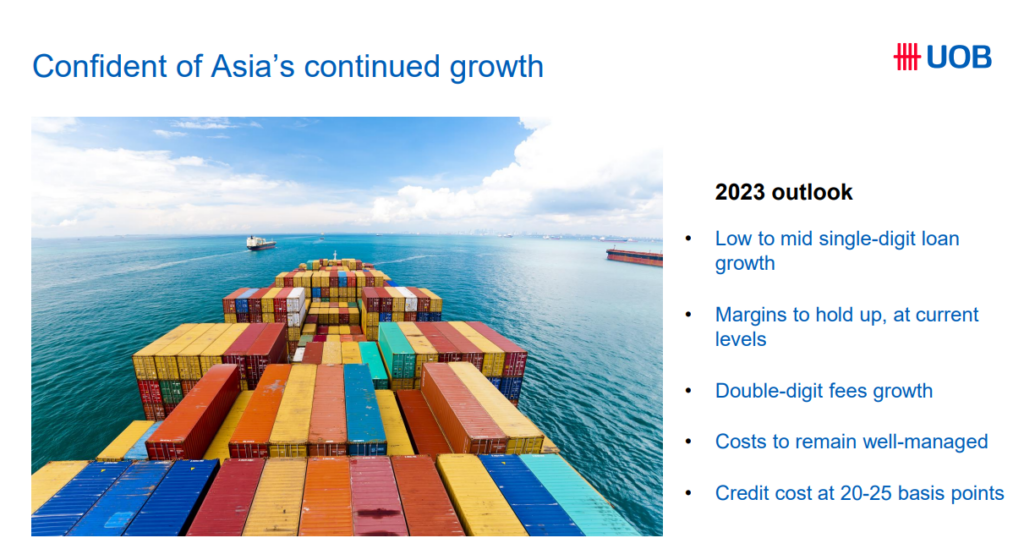

3. Growth outlook remains solid

Source: UOB’s Q1 FY2023 CEO Presentation

UOB’s management maintains an optimistic outlook on its growth prospects following the Citibank acquisition and is confident in achieving double-digit fee income growth while maintaining a favourable asset quality outlook.

However, management provided lower guidance on loan growth to low-single-digit while NIM is expected to be at around the 2.1% to 2.2% level for FY2023.

Loan demand could also be affected by higher interest rates.

Singapore banks resilient despite recent turmoil

The Singapore banks have remained resilient despite the turmoil seen in the banking sector in March.

The banking crisis, which was triggered by the failure of two US small banks, have led investors to take a deeper look at the banking sector.

Singapore banks have held up relatively well given the banks’ solid capital, liquidity ratio and risk management standards.

While UOB’s earnings in the near-term is likely to be supported by the integration of Citibank’s retail business, higher NIM, resilient loan growth and stable NPL, I believe most of the upside for UOB has been priced in.

In fact, the downside risks remain in the event of a contagion effect from the collapse in the US banking sector while a global recession could dampen its loan growth outlook further.

Long-term investors may find UOB attractive given its fair valuation of price-to-book of 1.03 times, which could earn a dividend yield of 4.8%.

While the uncertainties and risks in the near-term could hurt UOB, I believe the Singapore banks are supported by its resilient asset, solid balance sheet position and growth opportunities in Asia.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.