Get the ULTIMATE guide on how to invest successfully in Singapore REITs + our Top 5 S-REIT picks! Download now

Buckle Up for More Volatility in Stock Markets. Here’s Why

July 19, 2021

For investors in stock markets, Goldilocks is likely to get increasingly grumpy. And it is not quite because things are going badly.

It will more likely be because things are not going “Goldilocks-perfect”. Remember that Goldilocks-perfection requires a clear path out of the pandemic.

That equates to a strong economic recovery; robust corporate earnings growth; modest inflation; maintenance of central bank asset purchases at current rates; and zero policy rates in the Developed Market economies.

That’s an awful lot of stars to align perfectly, and the problem now is the bar to satisfying the market’s expectations has been set very high.

Delta variant messes up plans

There will likely be increasing gloom over the path out of the pandemic. It’s not because the Delta variant is a game changer.

In fact, it has been understood for some time that the path out of the pandemic was going to be long and painful, with more infectious variants competing with vaccine rollouts.

The data suggests that overall, the virus is less lethal now than at its early stage. The global mortality rate relative to the number of cases is much lower than at previous peaks.

And the path out of the pandemic remains the same – widespread vaccination, effective treatments, and herd immunity.

But for now, we are looking at another surge in cases and deaths. The decline in infections from May of this year appears to have ended.

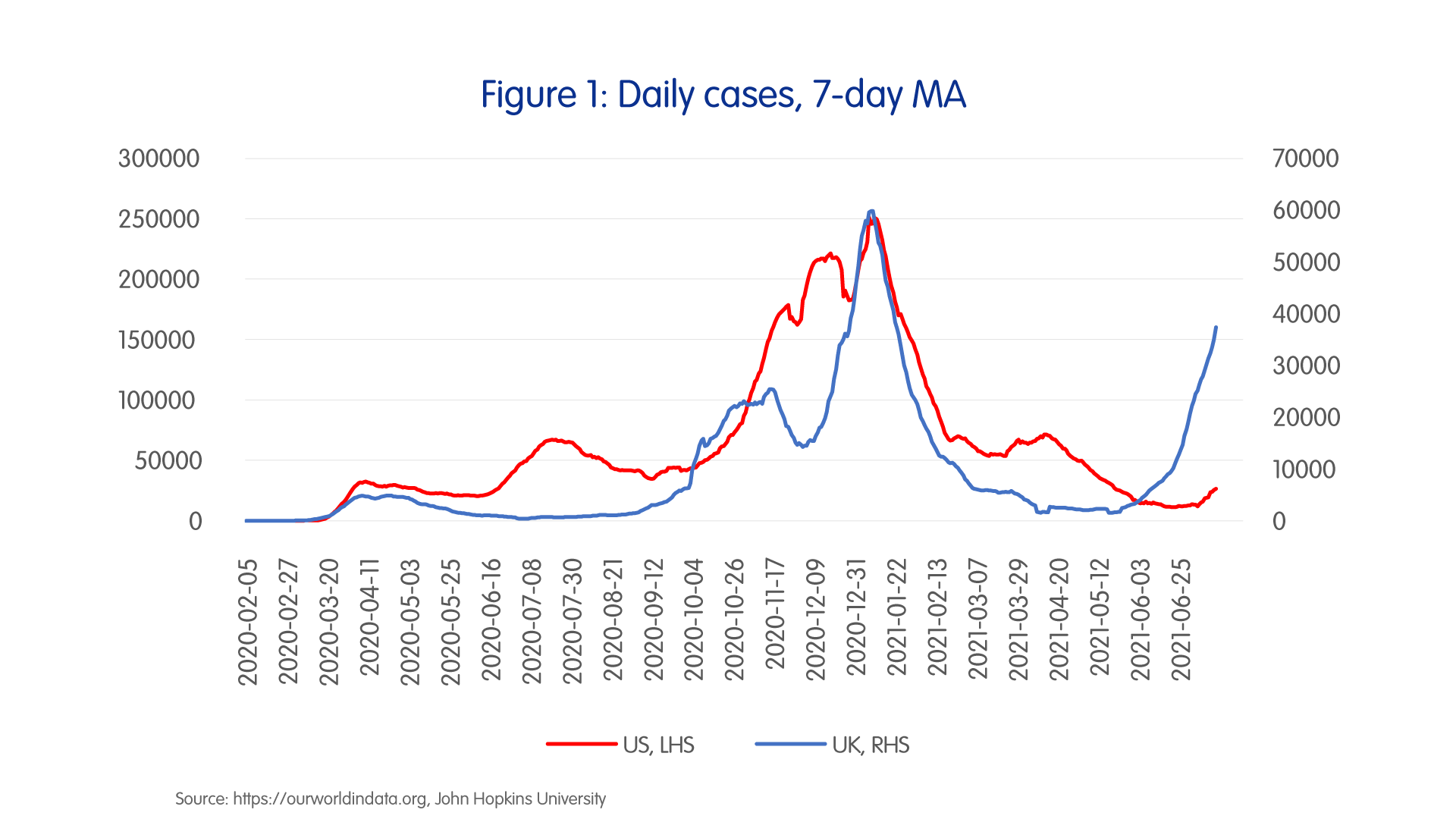

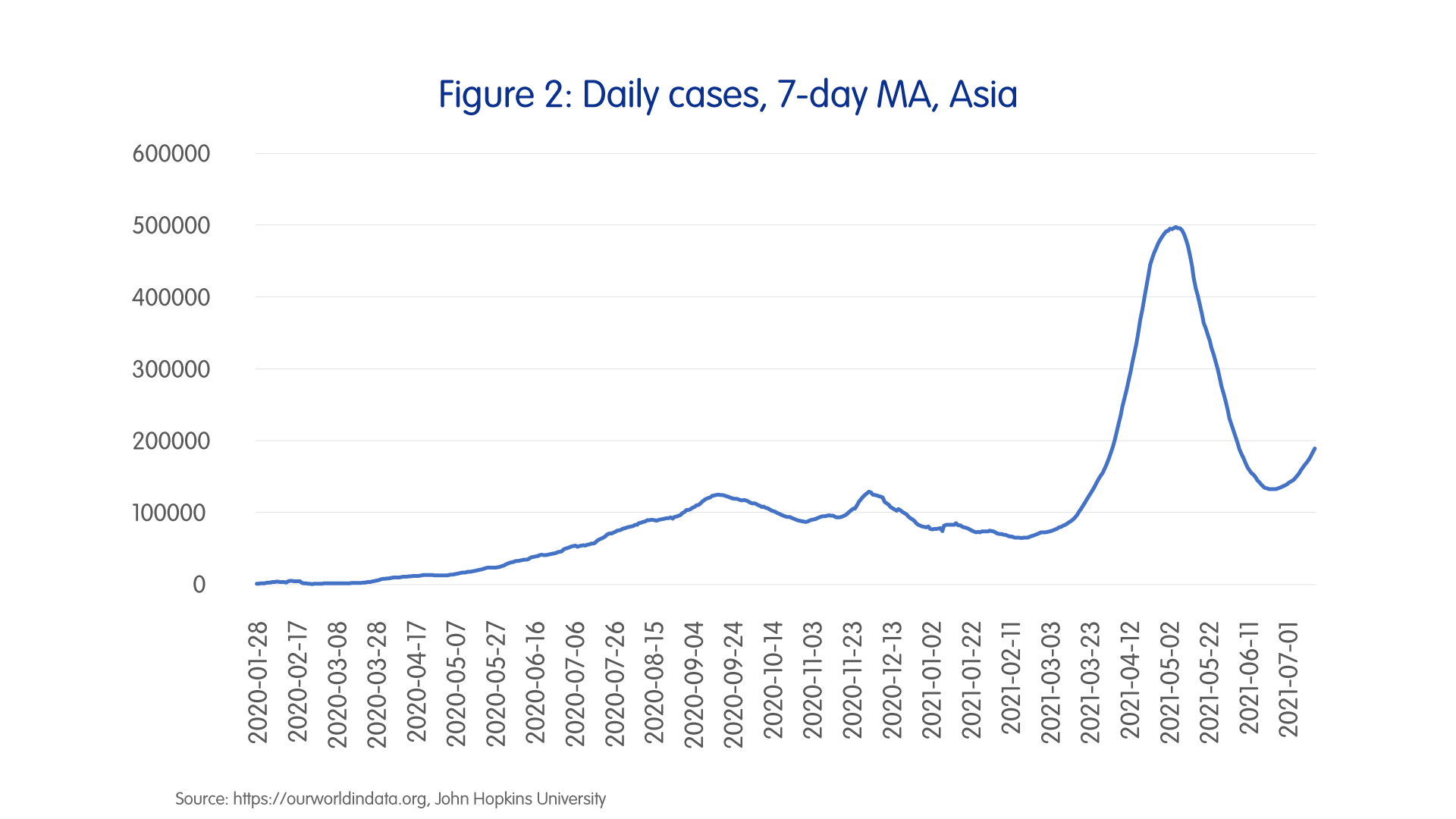

A new wave of infections may have already started at the aggregate level. Infections are surging in the UK, raising the likelihood of a similar surge soon in the US.

Case numbers are also turning in Asia (see figure 1 and 2). This will slow or temporarily halt reopening.

Narratives will wear thin

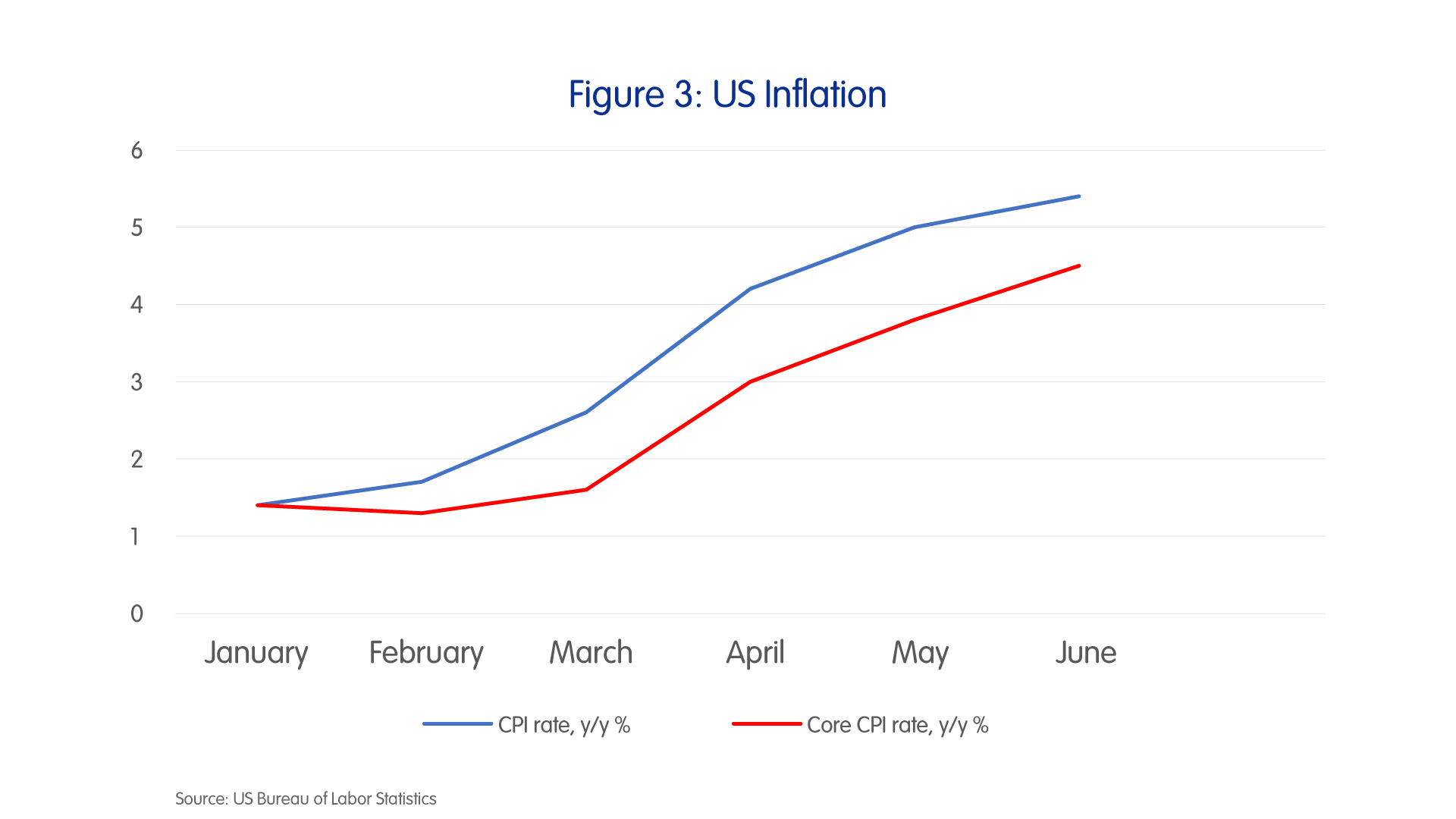

The Federal Reserve and US Treasury continue to chant the “it’s transitory” mantra. And that may well be the case, depending on what one’s interpretation of “transitory” is.

But US inflation – both headline and core – has not taken a single backward step since the start of the year (see figure 3).

Are we at peak economic growth?

While economies are rebounding strongly, that recovery is already in the price. And as we progress through the second half of 2021, the markets will look more at the slower economic growth rates expected for 2022.

The markets will be looking for signs of upside surprises for year 2022 economic growth rates. But the OECD Composite Leading Index (CLI) has surged to levels from which it will be challenged to exceed – these are historical highs.

So, we are likely to have seen peak economic growth. Against that, we may have also seen peak stimulus.

The US fiscal deficit relative to GDP is already at its highest since World War 2. The M2 money stock to GDP ratio is at a historic high, while M2 year-on-year growth has been declining since February this year (see figure 4).

Boosting stimulus will be tricky, both politically and financially, given the need to hold down inflation rates and bond yields.

Corporate earnings may also have peaked

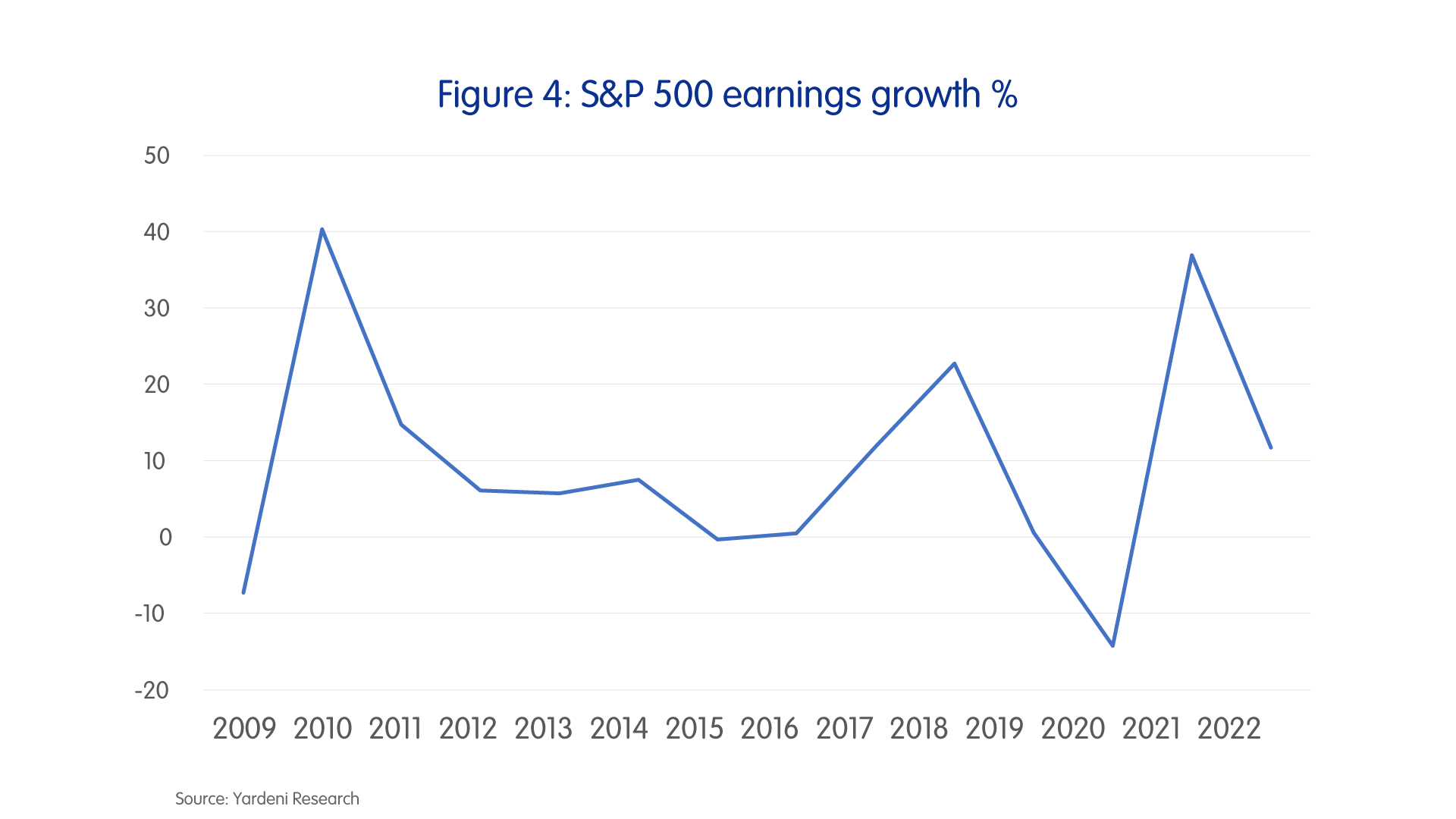

Just as we have seen peak economic growth, we have likely also seen peak earnings growth. The market is expecting 37% earnings growth for 2021.

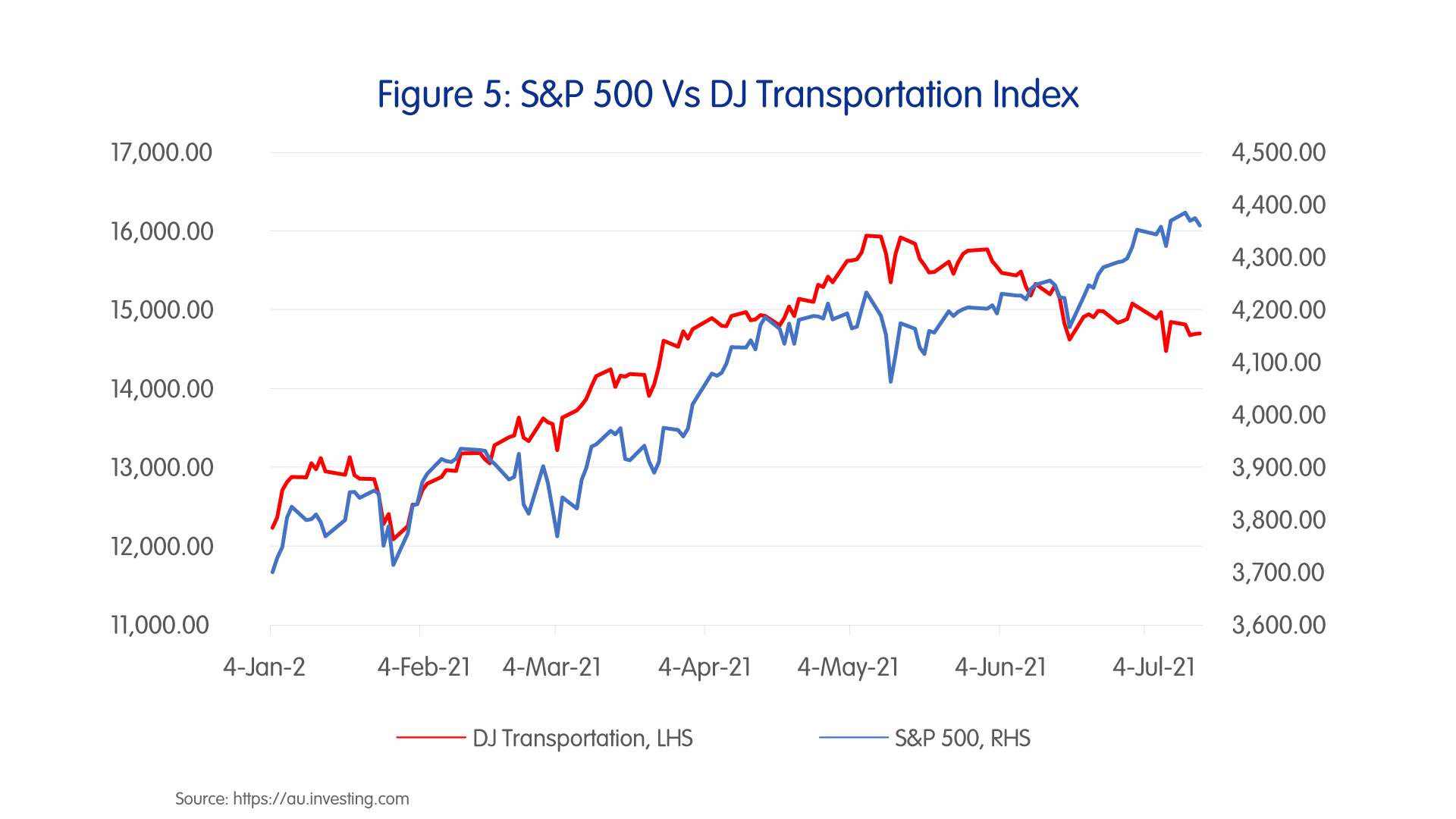

This is almost at the 40% growth peak post the Global Financial Crisis (see figure 5).

Correction, not the end of the bull market

With still a sizeable gap between the 10-year US Treasury yield versus most equities indices earnings yields, there is likely to be a tendency for funds to re-enter the market on dips.

Given we do not expect the first US rate hike until late next year, and particularly if the 10-year UST yield remains tame on an easing of economic leading indicators, there will be little incentive for investors to stay in cash for very long.

But Goldilocks may be about to throw a tantrum

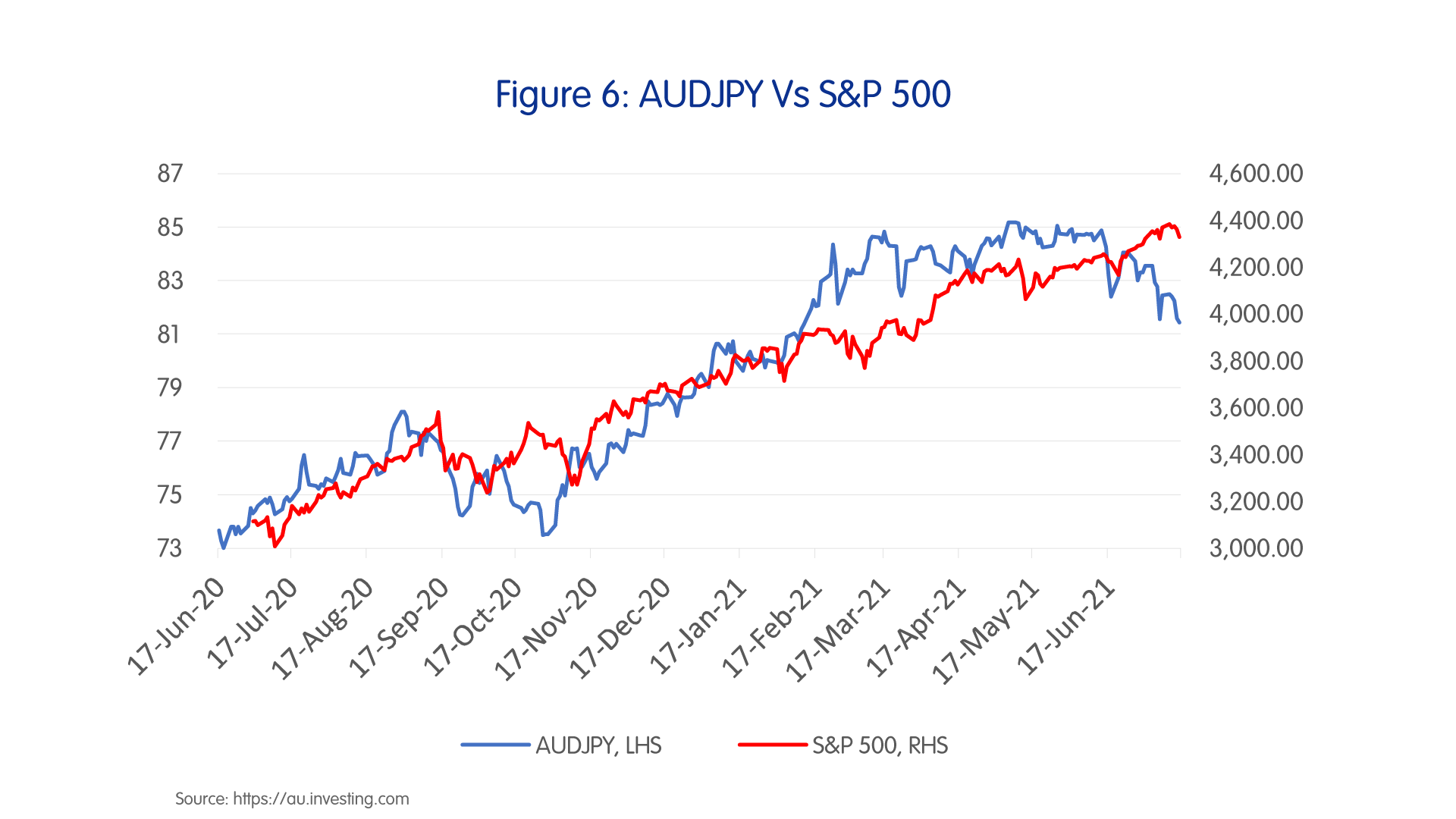

There are hints of market discontent in the divergences between the S&P 500 and the Dow Jones Transportation Index (see figure 6) and the S&P 500 against that risk-on/risk-off currency pair AUD/JPY (see figure 6).

So, for Goldilocks, the porridge may soon be too hot, the chair too big, and the bed too hard. There will be quite a bit in coming months to disappoint a market expecting perfection in a still very troubled world.

Say Boon Lim is CGS-CIMB's Melbourne-based Chief Investment Strategist. Over his 40-year career, he has worked in financial media, and banking and finance. Among other things, he has served as Chief Investment Officer for DBS Bank and Chief Investment Strategist for Standard Chartered Bank.

Say Boon has two passions - markets and martial arts. He has trained in Wing Chun Kung Fu and holds black belts in Shitoryu Karate and Shukokai Karate. Oh, and he loves a beer!