Get the ULTIMATE guide on how to invest successfully in Singapore REITs + our Top 5 S-REIT picks! Download now

Buying into the “Pro-Cyclical” Rally and Rotation Trade

July 8, 2021

The H1 2021 equities scoreboard validates the “rotation trade” that the CGS-CIMB Research team has been recommending.

And looking forward, despite the surge in the more infectious, so-called “delta variant” of COVID-19, the rotation out of US tech and consumer discretionary towards financials, energy, industrials, and real estate should continue.

This will happen on the back of what we had called “pro cyclical inflation”. For the record, the S&P 500 hit new highs in mid-June, to lead the major Developed Markets in gains for H1 2021.

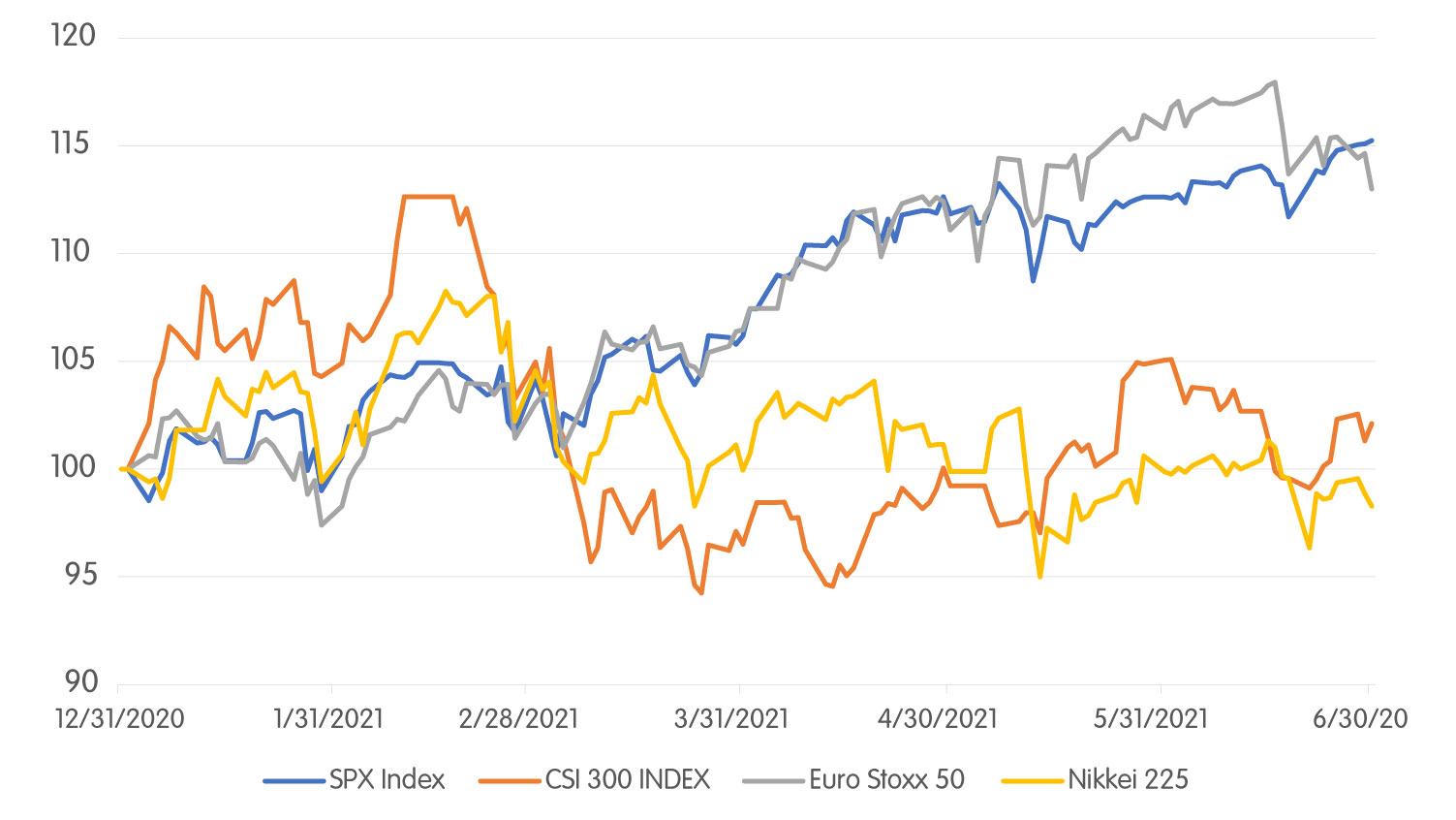

The S&P 500 ended the first half of the year up 15%. The Eurostoxx 50 was up 13% and Japan’s Nikkei 225 was down 1.7% for the first half. (see Figure 1 below).

Source: Bloomberg

And as we had said, Developed Market stocks can push yet higher despite moderately higher inflation, given strong economic and earnings growth.

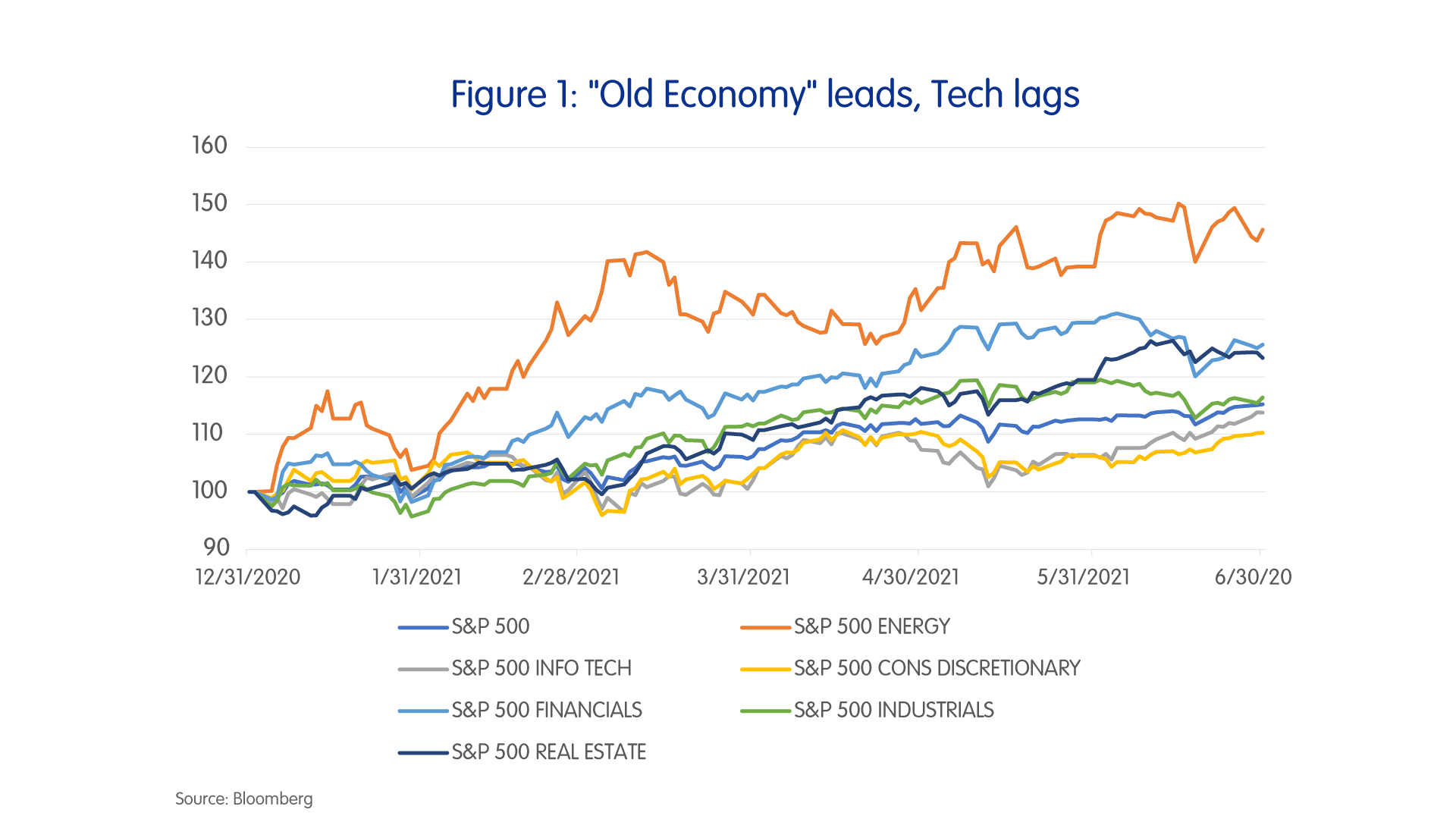

Rotation to “old economy” from tech continues

Within US equities, the worst performers were the beneficiaries of “Stay-home”/”WFH” – the tech and consumer discretionary sectors. The big winners were beneficiaries of a reopening of societies and economies – energy, financials and real estate (see figure 2 below). This was the rotation trade.

Looking ahead, the US equities market will likely see tech and consumer discretionary continue to lag. Gains in the broader market will likely be very much more selective in H2 2021.

Energy will depend more on production control than on demand recovery, which will be pushed back and forth by reopening in Developed Markets versus continued virus spread and low vaccination rates in Emerging Markets ex-China.

But on balance, oil majors are likely to see further gains on suppressed production. Financials and insurers are likely beneficiaries of expectations of higher rates and yields.

Cutting through the noise

The two big issues for H2 2021 are the path of the pandemic and inflation. The daily media reporting is very noisy on these issues and can be contradictory – depending on who you read and on what day.

Yes, the delta variant is more infectious than earlier variants. And at this stage, the scientific research is inconclusive on whether it causes more severe illness. That is, whether it is more deadly.

But vaccinations are being rolled out. And even if some of the vaccines have only 60-70% effectiveness in preventing infection of the new variants, they are still believed to be effective in preventing severe illness in over 90% of cases.

So eventually, as vaccines are rolled out, economies will gradually reopen, with infections continuing but becoming less severe. If that thinking is correct, the reopening and rotation trades should continue.

And with reopening of societies, economic recovery should gather pace, putting more upward pressure on prices. But there is still slack in labour markets.

So, the advance in prices will take time to gather sufficient momentum to force Developed Market central banks to act on rates.

As we have said before, the US will probably only hike rates towards late 2022. That buys equities quite a bit more time.

Say Boon Lim is CGS-CIMB's Melbourne-based Chief Investment Strategist. Over his 40-year career, he has worked in financial media, and banking and finance. Among other things, he has served as Chief Investment Officer for DBS Bank and Chief Investment Strategist for Standard Chartered Bank.

Say Boon has two passions - markets and martial arts. He has trained in Wing Chun Kung Fu and holds black belts in Shitoryu Karate and Shukokai Karate. Oh, and he loves a beer!