Here’s How the Russia-Ukraine Conflict Will Impact Your Portfolio

February 26, 2022

Geopolitics do not typically change the underlying trend in stock markets, unless the event significantly alters dynamics in the economy.

Where the underlying tendency is bullish, negative geopolitical events – including wars – disrupt but do not derail uptrends.

Where the underlying tendency is bearish, these events tend to accelerate the downtrend – sometimes with tradable rebounds in between (given the speed of those accelerated declines) but with eventual returns to those downturns.

Markets already struggling before invasion

Valuations were already stretched for specific markets, particularly US tech stocks. The S&P 500 was already trading on a forward price-to-earnings (PE) ratio of around 22x in early January when the index peaked.

These are cyclically high valuations, comparable to levels hit in the late 1990s, in the leadup to the 2000 Tech Bubble Crash. US stocks were priced for perfection.

But underlying conditions have been far from perfect. Let’s take a look at why the markets have been under pressure:

- This was a bull market perversely created by an extremely adverse event – a once-in-a-century pandemic which pushed governments into unprecedented fiscal and monetary stimulus

- That stimulus is reversing into policy tightening

- Inflation is raging in the US and the Euro Area

- Rates are set to rise and,

- US earnings growth is flattening out from around 49% last year to an expected 8% for this year. Given US inflation is currently running at 7.5%, there is a prospect of near-zero real earnings growth this year

Stock market declines likely to accelerate

The Russian invasion of Ukraine will add to the hurdles facing stock markets if sanctions imposed on Russian commodities add to inflationary problems.

While the market usually focuses on US economic data, it is worth noting Euro Area Producer Price Inflation was already up an eye-watering 26% year-on-year in December.

The S&P 500 Index had already fallen out of its uptrend from April 2020, weeks before the Russian invasion (see Figure 1 below).

Figure 1

Source: Refinitiv

And it was looking unlikely that it would recapture that uptrend, given rising rate expectations mirrored by the Fed Funds Futures markets, as well as rising government bond yields and corporate credit spreads.

With the war in Ukraine, only the most optimistic investor will still hold that hope of a return to an uptrend.

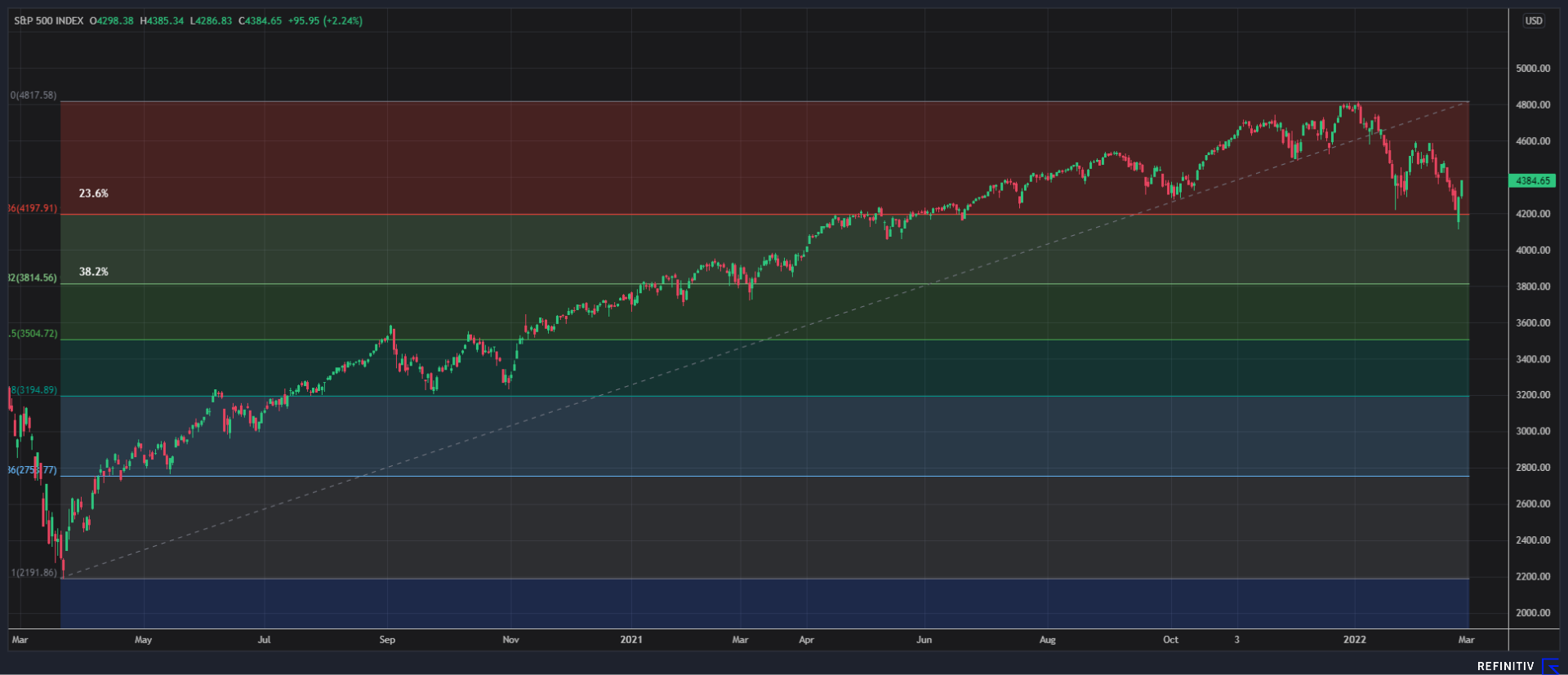

Going forward, I would expect a near-term, technical rebound for the S&P 500 at around the 4,200-4,300 support zone.

This was the area which saw rebounds in July and September-October of last year. And it is important that the S&P 500 holds up above this zone.

But I fear the odds are growing of a break below this level – which also coincides with the 23.6% Fibonacci retracement of the entire move from the March 2020 low to the January 2022 high.

A break below this risks the acceleration of losses towards 3,820 which coincides with both the 38.6% retracement level and the approximate “head and shoulders” target following the break below the “neckline” at around 4,350 (see Figure 2 below).

Figure 2

Source: Refinitiv

In short, there is still considerable risk in trading any rebound in the next week or so. A possibly stronger support level for tactical longs might be closer to the 3,820-region.

And that, by the way, will take the S&P 500 down around 20%, brushing up against bear market territory.

Ironically, that may be the time for the bulls to come out; just when the sellers capitulate into an “official” bear market.

By the way, at that level, the S&P 500’s forward PE ratio – on assumption of unchanged consensus forecast of index earnings of 223 – will revert back to around 17x.

That would see the index valuation back to the more reasonable levels of mid-2020.

No stocks will be spared in risk-off mode

When the world’s largest markets – the US and Europe – are dumping risk because of the rising risk-free rate and the addition of a geopolitical risk premium, most asset prices are affected.

So, outperformance is only in relative terms. Yes, my preferred global value trade is outperforming still, but only in reducing the losses.

Stick with energy and commodity players

Even energy and commodity producer stocks have suffered price declines over recent days. And that may seem particularly counter-intuitive for oil majors given the surge in the price of crude oil.

One reason is the sanctions announced so far have not touched Russian energy exports. Another is the expectation that a deal between the US and Iran could see the lifting of sanctions, resulting in the return of Iranian production and inventories.

In a nutshell, I still see higher energy prices and oil stock prices in coming months. The inventories held by Iran are only around 1% of known inventories around the world.

Its 3.8 million barrels/day production capacity will ease the tightness of supply but may not see supply exceeding robust demand.

Finally, there is a risk of Russia cutting off gas to Europe in retaliation for financial sanctions. I would stick with buying into selected oil majors and commodity producers as beneficiaries of rising inflation.

Europe outperformance could struggle

Unfortunately, Europe, which I had preferred as a lower rates/yields alternative to the US market, is now falling as much as its American counterpart year-to-date.

The Euro Stoxx 50 had indeed lost more over the past five days than the S&P 500, given the higher European geopolitical risk premium.

Unless the European Central Bank (ECB) dials down its rate hike talk – signaling a high degree of tolerance for inflation – European stocks will (at best) perform in line with US equities.

Japan likely an outperformer

The case for Japan’s outperformance is still valid, given its still muted inflation, the Bank of Japan’s very dovish communication on rates and yields.

There’s also the greater representation of value stocks on its indices, and its geographic insulation from the dangers in Eastern Europe.

China stocks making a comeback?

China’s CSI 300 Index has suffered lower losses than the S&P 500 year-to-date, with relative outperformance more noticeable since the start of February.

I would maintain my outperformance view of Chinese equities given their low relative valuation, ongoing policy stimulus, and China’s political and geographical distance from the problems entangling the US, Europe and Russia.

However, Chinese stocks still suffer from considerable policy risk as it continues with the regulation of its tech sector and other supply side reforms.

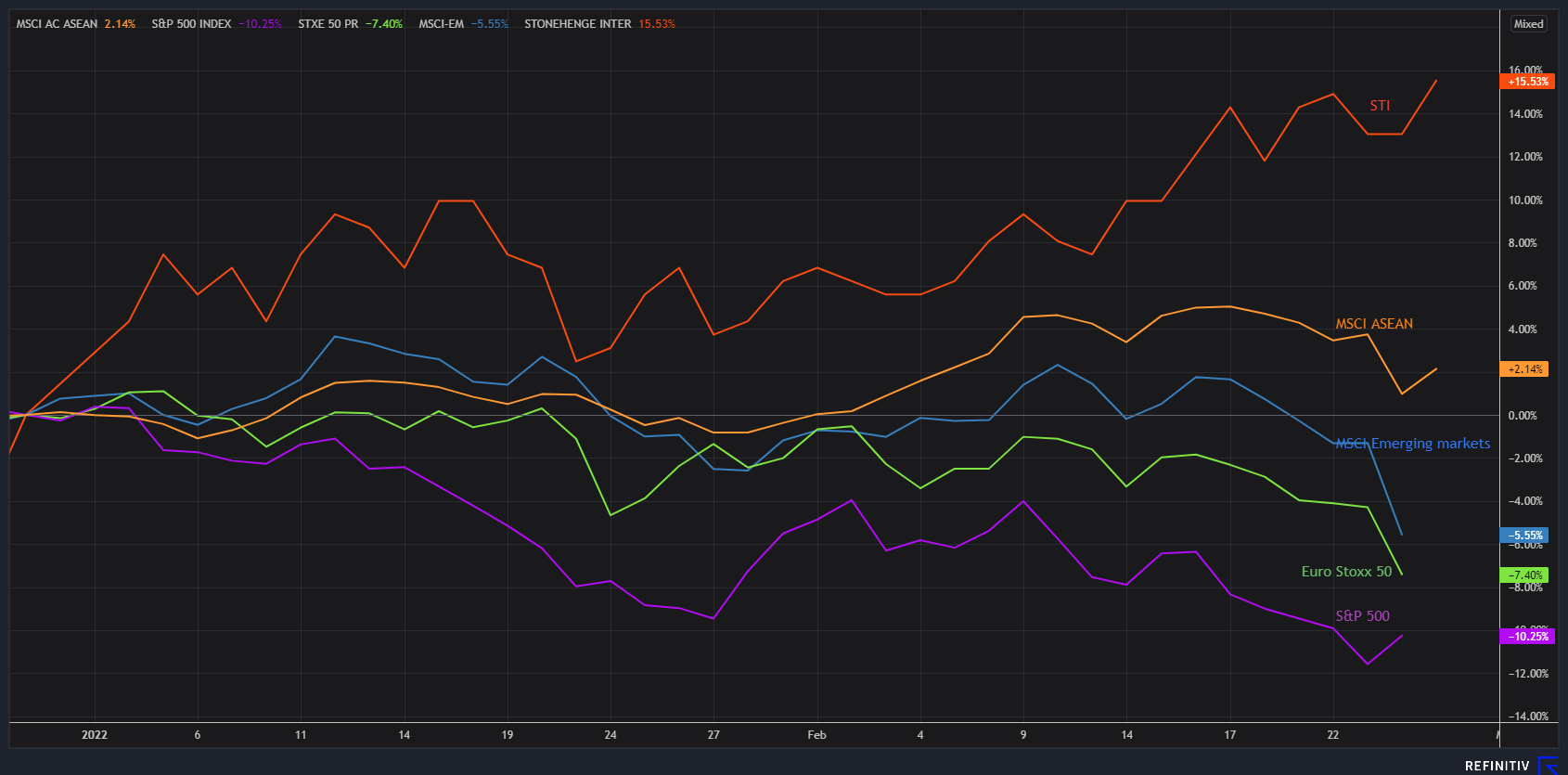

ASEAN/Singapore stocks as a value play

In the search for alternatives, interestingly, ASEAN could emerge as a value sector outperformer. The MSCI ASEAN has indeed been one of the few regional indices that have turned in positive returns year-to-date.

And that has been driven in large part by my favorite ASEAN market – the value play Singapore market (see Figure 3 below). I would recommend continuing to buy Singapore stocks on the dip.

Figure 3

Source: Refinitiv

Say Boon Lim

Say Boon Lim is CGS-CIMB's Melbourne-based Chief Investment Strategist. Over his 40-year career, he has worked in financial media, and banking and finance. Among other things, he has served as Chief Investment Officer for DBS Bank and Chief Investment Strategist for Standard Chartered Bank.

Say Boon has two passions - markets and martial arts. He has trained in Wing Chun Kung Fu and holds black belts in Shitoryu Karate and Shukokai Karate. Oh, and he loves a beer!