Get the ULTIMATE guide on how to invest successfully in Singapore REITs + our Top 5 S-REIT picks! Download now

Inflation: Hedge, Rotate and Discriminate

May 27, 2021

The hot topic in markets right now is inflation. Is it “transitory” as the Fed assures us or is it history? Let’s cut to the chase – it is likely to be persistent and significant. And it will have important consequences for investment strategies.

The latest inflation print for April out of the US was undeniably robust. And the Federal Reserve (Fed) likely knew this was coming, hence its softening the ground with repeated assurances that it would be “transitory”, even before the data landed.

Core inflation for April came out at 0.9% month-on-month, from 0.3% month-on-month in March. The last time we saw a higher figure was in 1982 – when then Fed Chair Paul Volcker was forced to take a hammer to break the back of US inflation.

The 12-month core inflation figure is now 3%, despite it including data from the worst months of the pandemic last year. This is up dramatically from 1.6% for the 12 months to March.

Three reasons inflation isn’t going away

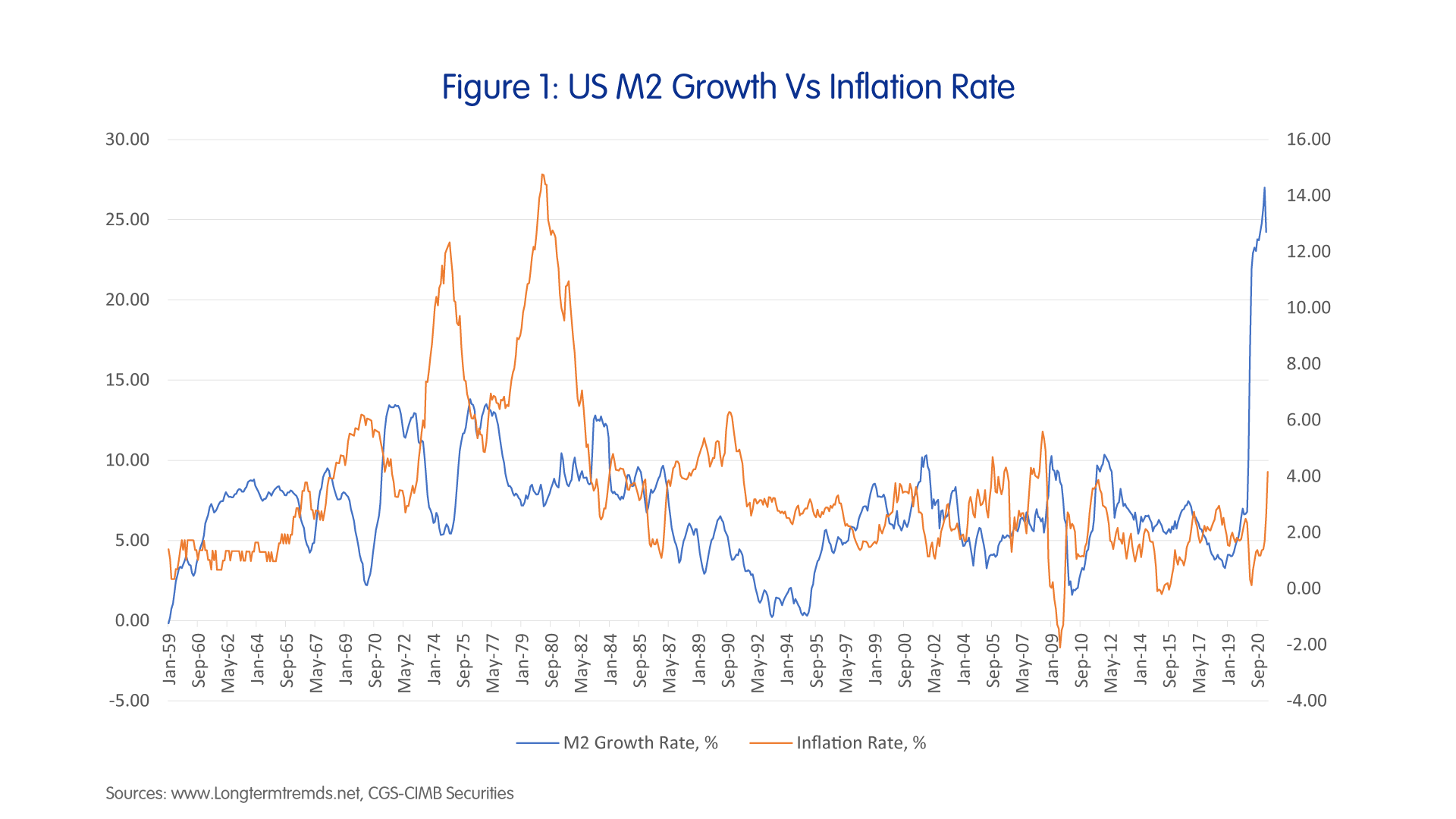

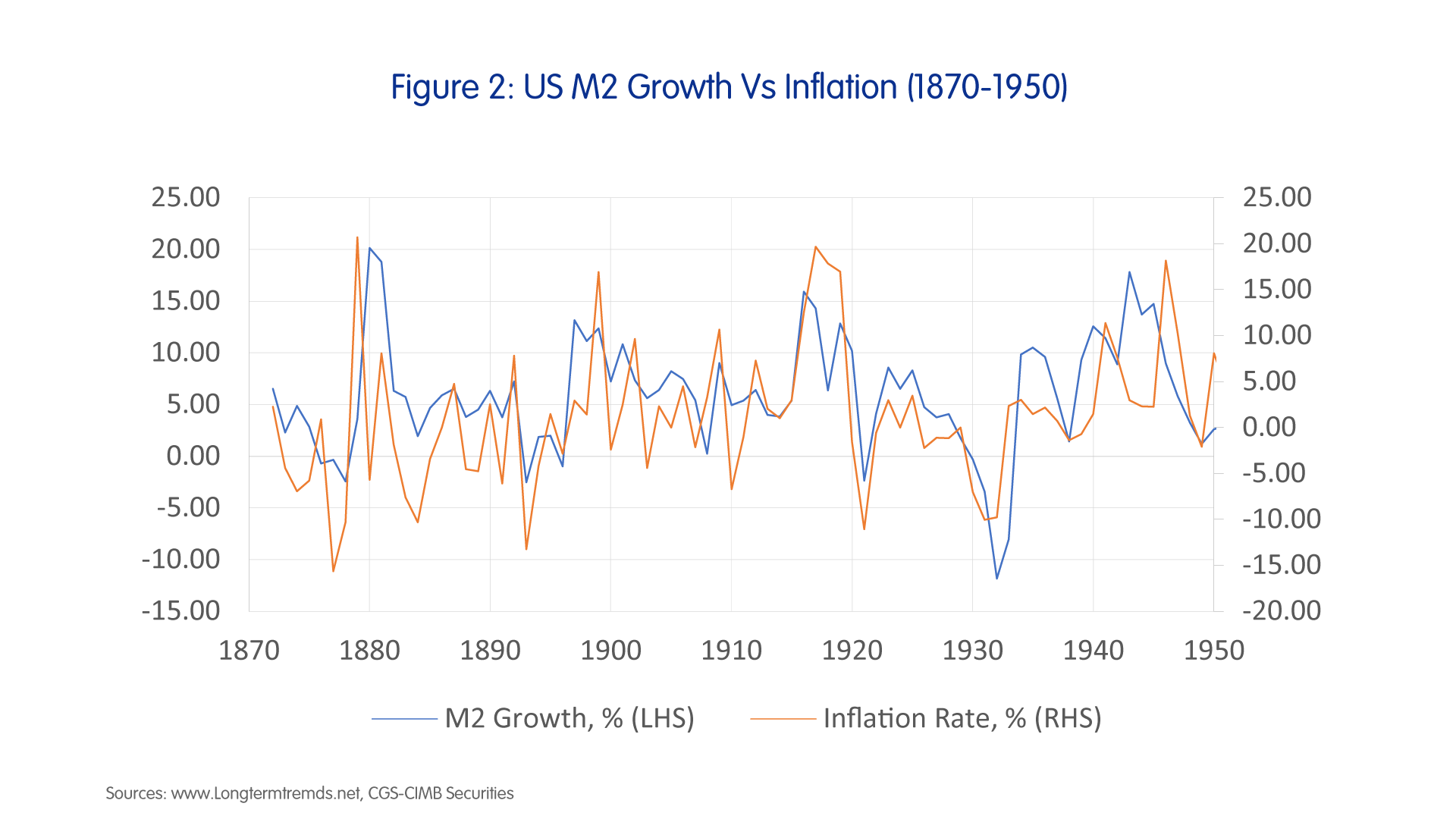

1. There is a long US history of high inflation following or coinciding with periods of high money supply growth (Figures 1 and 2 below).

We have seen this movie before, many times – during the so-called “Long Depression” of the 19th century; the “New Deal” stimulus of 1933-36; during the Second World War; and during the Vietnam War. Note the theme – monetary expansion to finance recovery from economic crises and wars.

And we are in the midst of an economic crisis and a “war” against a virus. So, since the start of last year, we have seen a period of the greatest monetary expansion in US history, and it isn’t even over yet. The US is still printing and handing out more money.

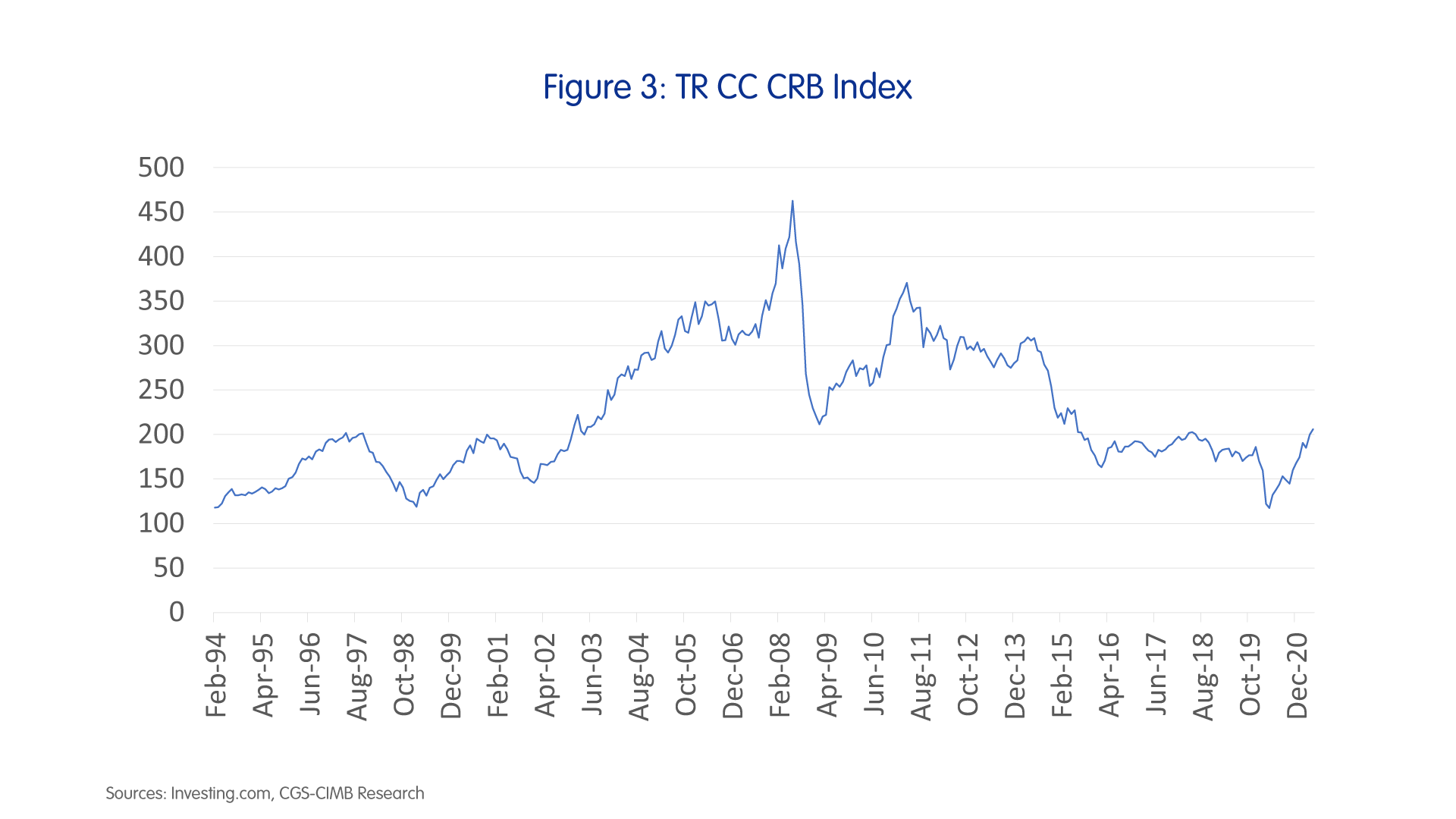

2. We now appear to be at the early stages of a new commodity cycle that started last year, with likely added vigour caused by fiscal stimulus in the world’s two largest economies, the US and China.

The infrastructure spending in these economies will likely drive competition for commodities, inventory building, and yet higher prices (Figure 3 below).

3. Supply chain disruptions caused by the pandemic and higher tariffs imposed by the US and China on one another will add that little bit more to prices.

Equities can tolerate higher inflation…only for a while

Equities will likely tolerate higher inflation in its early stages, while GDP and earnings are growing rapidly. Currently, the S&P 500 trailing 12-months (TTM) earnings yield is around 2.3% and the 10-year US Treasury (UST) yield is now around 1.6%.

Yes, this is a narrow “spread” but it will likely get narrower. The danger zone is likely where the 10Y UST yield and the TTM earnings yield intersects. Bullish next 12-months (NTM) earnings yields will also provide a further buffer.

There should be a difference between inflation in a rapidly growing economy and inflation in a slowing or stagnant economy. We are currently in the former. This is pro-cyclical inflation, rather than counter-cyclical inflation. Equities will likely tolerate inflation better when GDP and corporate earnings growth rates are high.

In the same vein, historically, US equities have tended to go up in the early stages of rises in the 10-year UST yield. At the later stages of the rise, problems emerge when higher borrowing costs choke off economic activity, and bond yields make equities no longer attractive. It is likely that we are not there yet.

Outlook for DM bonds is very worrying

The ultra-low spreads at the moment for both Developed Market (DM) investment grade and high-yield credits are a huge risk. It seems there is little room for spreads to move lower, but a lot of room for them to move higher, which can devastate bond mark-to-market values.

Five strategies: Hedge, rotate and discriminate

1). Forget about bonds unless you are holding high quality bonds to maturity.

2). Reduce exposure to tech stocks which are more vulnerable than “old economy” stocks to rises in rates and yields because a larger part of tech valuations are tied up in distant future earnings and terminal value.

3). Rotate from tech to “old economy” stocks such as financials, industrials, materials, energy and real estate.

4). Hedge through gold and commodities. Gold has had a good run since the start of April and is due for a correction. But our strategy is to buy the dips in gold. Ditto for commodities – buy the dips in base metals and agricultural products through diversified funds.

5). Discriminate within Emerging Markets. Favour markets in countries which have better management of the pandemic (remember it’s not over yet) and inflation, and with exposure to commodities.

China, Indonesia, South Korea and Australia

China has had one of the most effective pandemic management systems in the world and its consumer inflation is still tame.

Its GDP growth will likely be the highest of the major economies this year. And it has proven through the pandemic to be an indispensable hub of global manufacturing.

Indonesia currently has a COVID-19 infection rate lower than most Emerging Market economies, and comparable to South Korea. Its inflation has been tame and 60% of its exports are commodities.

South Korea has rising inflation but it is a special sector play on semiconductors – a digital economy “commodity” in short supply. Finally, Australia has almost eliminated the COVID-19 spread within the community, has a relatively well-behaved economy and is a commodity economy. The fact that it has a robust currency also helps.

Say Boon Lim

Say Boon Lim is CGS-CIMB's Melbourne-based Chief Investment Strategist. Over his 40-year career, he has worked in financial media, and banking and finance. Among other things, he has served as Chief Investment Officer for DBS Bank and Chief Investment Strategist for Standard Chartered Bank.

Say Boon has two passions - markets and martial arts. He has trained in Wing Chun Kung Fu and holds black belts in Shitoryu Karate and Shukokai Karate. Oh, and he loves a beer!